Recent bellwether corporate earnings reports are painting a very gloomy picture of the US and global economies this year:

- Microsoft lived down to expectations and delivered a gloomy outlook.

- GE missed, blaming its renewable energy division.

- Tesla beat on most metrics and offered very upbeat guidance (orders at 2x production).

- Sherwin Williams served up more gloom.

- Walmart, the world’s biggest retailer, was the 800-pound gorilla of gloom, adding that food inflation remains stubbornly in double-digits.

- Intel missed on almost every line—and delivered the gloomiest outlook of them all.

We’re also getting constant reports of layoffs by the thousands—and not just in the tech sector, where Apple, Amazon, and others are laying workers off. One particularly telling layoff came from toymaker Hasbro, which is laying off 15% of its workforce.

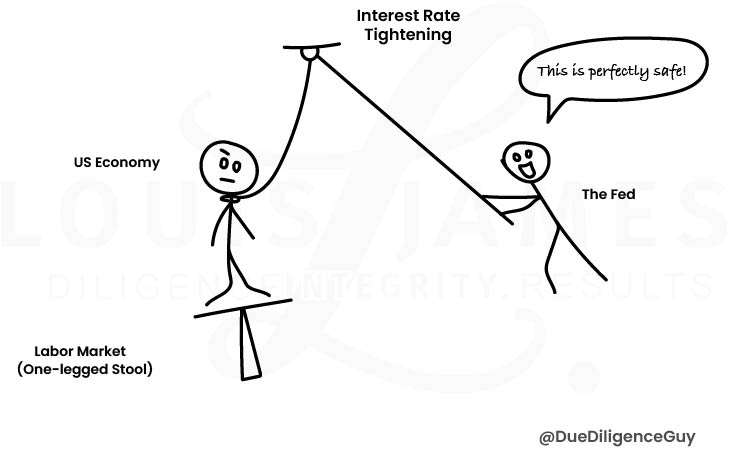

And yet US jobless claims remain very low—below 200,000 per week—and even continuing claims dipped in the last reading. This has FOMC members like Loretta Mester arguing for “soft landing” scenarios, in which the Fed can tame inflation without creating much unemployment.

I don’t agree.

Here’s why:

- It’s delusional to think that tech-sector layoffs will only affect the tech sector. Those people spend on goods and services—or they did. Hasbro decimating itself is particularly telling. Coupled with reports of lackluster holiday sales from many sources, that looks like a big red flag waving over the economy.

- Layoffs are announced before they happen; it takes time for them to show up in unemployment claims. Severance packages can greatly lengthen this lag.

- There are plenty of job openings, but a lot of them are flipping burgers… not something appealing to a software engineer. The lion’s share of the new jobs in the “blockbuster” January jobs report from the US are in services and hospitality. That’s a sector still in recovery from the COVID-19 lockdowns. And again, it’s not the same quality of work as the high-paying tech and manufacturing jobs the US is losing.

- Don’t forget that labor force participation remains historically low. Unemployment rates will look much lower than they really are if people just give up—as many reportedly are. I don’t think the high number of job openings is a sign of economic strength, but of deep economic trouble. Whatever else it means, those who drop out of the labor force will spend less.

- For equities in general, the sudden reappearance of “risk-free yield” (in short-duration treasuries) is a major, major headwind. And if stock markets continue grinding lower, the reverse wealth effect will be a millstone around the economy’s neck.

- The latest CPI (6.4% headline and 5.6% “core) and PCE (5.4% headline and 4.7% “core”) prints show much “stickier” inflation than expected.

- I can’t prove it, but I think that the US and global economies are far more fragile than most investors realize. I think they were before the COVID-19 lockdowns (hence governments’ panicked economic responses) and are all the more so now with the war and the New Iron Curtain.

Combine the expressed optimism from FOMC members that the Fed appearing can “beat” inflation without doing much harm to the economy with the Fed’s preferred measure of inflation surprising to the upside…

The odds just went up that the Fed will “break something.”

A key thing to remember is that while most investors seem obsessed with the Fed’s rate hikes, so-called quantitative tightening (QT) is going on in the background.

Rather than admit to a premature victory lap, Powell and the FOMC may well stick with 25-basis-point rate hikes at its next meeting(s). But QT will still be draining liquidity from markets addicted to easy money.

Until the labor market breaks.

I realize that sounds like a prediction, but I’m not saying I know what will happen; I’m saying that this seems to be the most likely outcome.

If I’m right, the “Fed pivot” markets are now not expecting until next year is likely to arrive this year—easily by this summer.

But it won’t be because the Fed has beaten inflation; it will be because the Fed has had to give up the fight in order to save the economy.

Easier money may or may not boost mainstream stocks. Depending on how bad the recession looks, it may not boost commodities prices until after a long lag. But it should be very good for monetary metals: gold and silver.

Meanwhile, buckle up for more volatility—and prepare to make it your friend.

![]()

P.S. To be kept abreast of my ideas for how to make volatility our friend, please sign up for our free, no-hype, no-spam Speculator’s Digest.