It’s become fashionable in financial media to try to debunk gold’s status as an inflation hedge—a status that has endured for centuries.

A recent CNBC article claimed that history suggests that gold is not a good hedge against inflation. The author’s “historical” context was that gold prices fell during inflationary periods in the 1980s. Given the thousands of years in which gold has been the best store of value in the world, this strikes me as cherry-picking the data.

Still, I can understand why people might ask. In our most recent interview, Kitco’s David Lin did just that, as he’d run the correlation between gold and CPI over the last 10 years and found almost no relationship.

The first answer that jumps to mind is that CPI is a terrible measure of inflation.

But lousy as it is, CPI does measure some price increases, so we can’t ignore its relationship with gold entirely.

A more useful answer is that timeframes matter.

We’ve seen in recent years that inflation expectations can have a dramatic impact on gold prices (David had a chart for that in our interview as well). In other words, gold often leads actual inflation.

Think about what that would do to correlation coefficients…

- If gold rises before inflation (as over the last year), there would be little or no correlation between the two during that timeframe.

- If gold is then flat or loses altitude when inflation picks up—having already priced inflation in, in advance—there would again be little or no correlation between the two.

- But gold would still have served as a hedge against inflation.

This is why I told David that timeframe is everything.

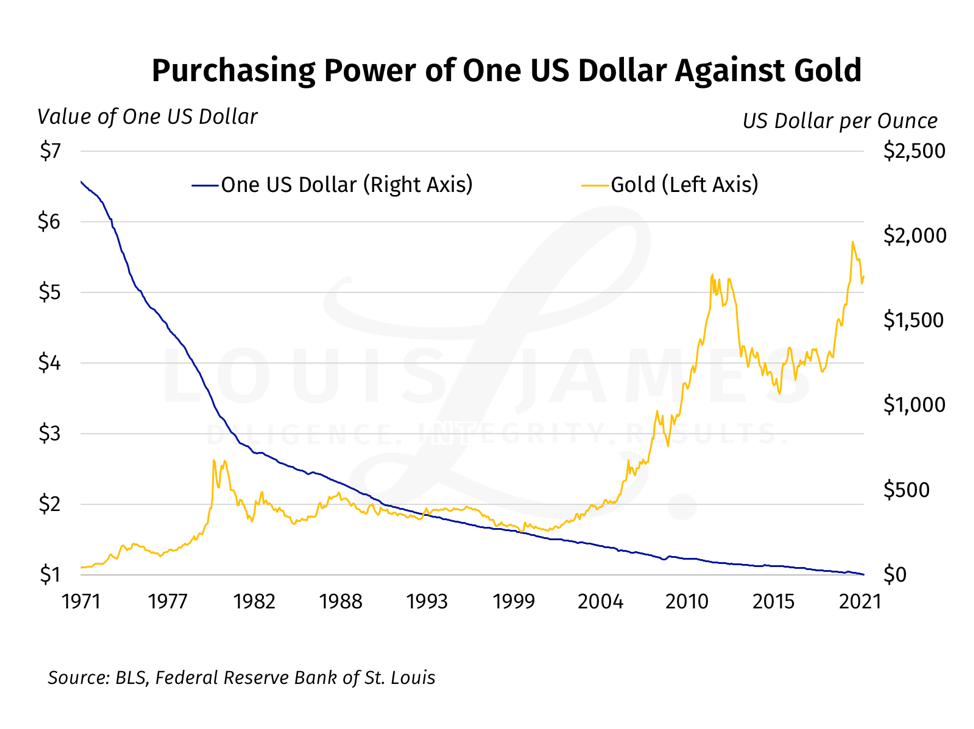

And it’s why I think the most relevant—non-cherry-picked—timeframe for this question is 1971 to present. That’s our modern monetary era. It started when the US dollar was completely severed from the gold standard by Richard Nixon, allowing gold to trade freely. Or, as unintended consequences have a way of doing, allowing the gold-dollar exchange rate to show the deteriorating value of the USD.

Here’s that chart…

Note that this uses CPI to measure the USD’s loss of purchasing power, which I think vastly understates the loss. There’s also a methodological issue with comparing gold priced in dollars to CPI-adjusted dollars.

The fact remains that it takes $6.55 today to buy what $1 bought in August of 1971, when Nixon turned the USD into a floating abstraction—and the price of gold is up about 54x in that same timeframe.

That’s according to the US government’s inflation-minimizing (in my opinion) statistics, of course.

Keep this in mind whenever anyone tells you that gold is no hedge against inflation.

Also remember the thousands of years of history in which gold and silver have been the world’s best means of wealth preservation.

That’s my take,

![]()

P.S. To be kept abreast of more dangers, opportunities, and issues affecting investors, please sign up for our free, no-spam, weekly Speculator’s Digest.