Lobo Tiggre

Last year revealed something I suspected, but had no measure of… until now.

You see, I’ve long advocated a calm, value-oriented approach to resource speculation. As Buffett says, opportunities exist because people don’t want to get rich slow. Hence my mottos: “Discipline pays” and “caveat emptor.”

This approach is self-evident in a bear market. It’s less obvious when a new bull awakens and climbs the inevitable wall of worry—but my report cards show that I beat the market at such times (click here for: 2022, 2023, and 2024). What I suspected and now have evidence for is that my cautious approach may underperform in a mania.

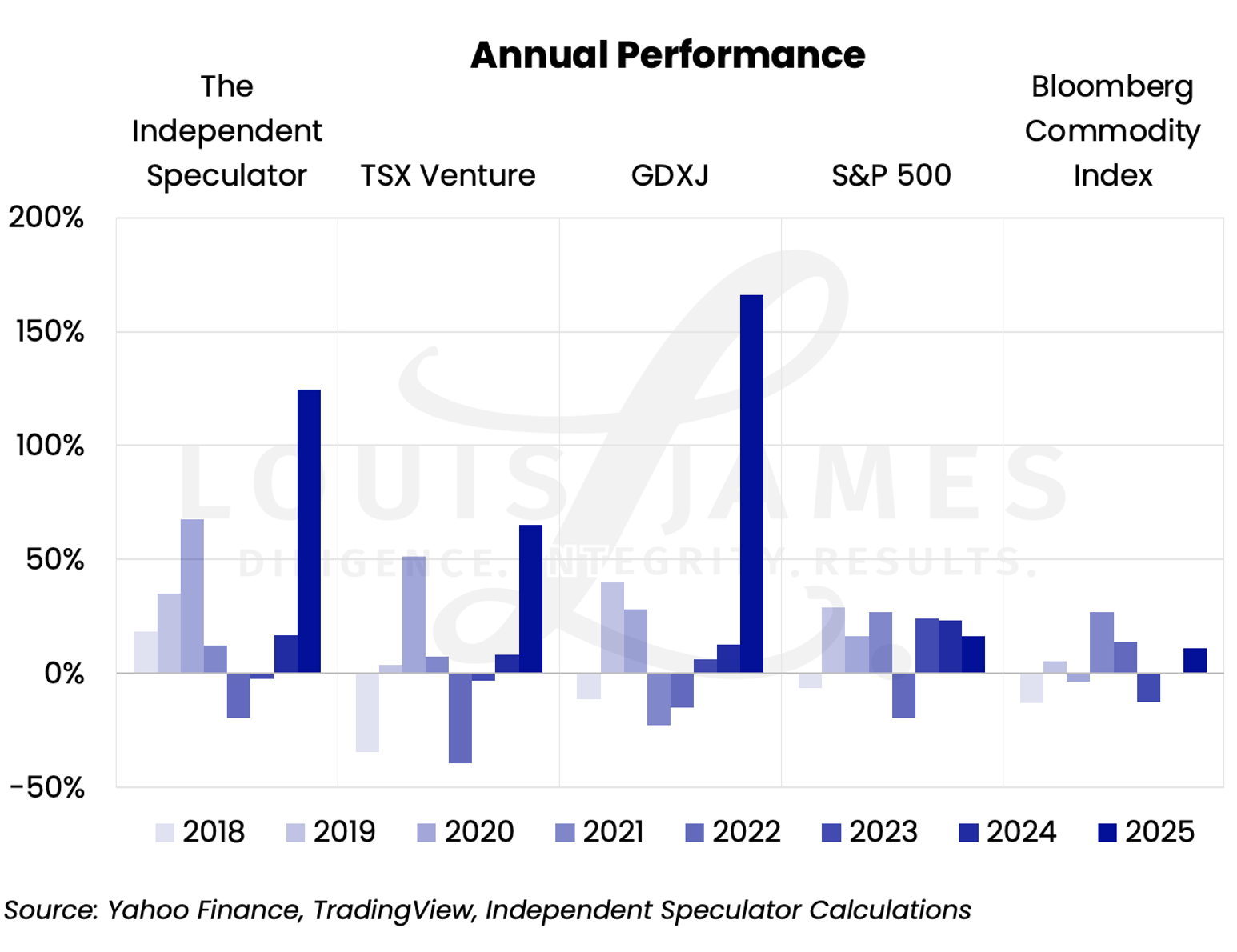

Here’s how my picks in The Independent Speculator did:

As you can see, I beat the broader markets in 2025, but for the first time, the GDXJ beat me.

Mind you, it’s not that I had a bad 2025: my portfolio was up 124.55% for the year. It’d be up 133.97% if we didn’t count my recent purchases that didn’t have a whole year to rally. This brings the average yearly performance since inception of The Independent Speculator up to 31.6%.

Also, a client wrote in to say that I shouldn’t compare The Independent Speculator’s annual results to the GDXJ because that’s based on gold and silver, while my portfolio has uranium, copper, and oil in it. It’s a fair point, but I’ve long used the GDXJ as a benchmark, and I don’t want to be seen as moving the goalposts. That said, it’s true that if we consider my gold and silver picks only, they averaged 197% in 2025, beating the GDXJ’s 166% handily.

Still… It’s eye-opening to be outperformed by an index that includes companies I don’t think highly of.

But this does make some sense. In a manic market, crappy companies can outperform in share price appreciation because they see the most margin improvement. They are riskier, but when prices are going vertical, it’s hardly surprising to see Mr. Market throwing caution to the wind. (For more on this, see my article on marginal producers.)

There’s evidence of this in the data showing how My Take did in 2025. Here’s a breakdown of the companies we cover, by major commodity:

| Count | Claws-Up | Claws-Down | Total |

| Total | 117 | 985 | 1102 |

| Gold | 62 | 469 | 531 |

| Copper | 15 | 118 | 133 |

| Uranium | 14 | 68 | 82 |

| Silver | 6 | 91 | 97 |

| Oil & Gas | 11 | 42 | 53 |

Now here’s how my claws did:

| Average Performance | Claws-Up | Claws-Down | Total |

| Total | 108% | 134% | 131% |

| Gold | 150% | 152% | 152% |

| Copper | 121% | 135% | 133% |

| Uranium | 32% | 16% | 19% |

| Silver | 179% | 196% | 195% |

| Oil & Gas | 8% | 8% | 8% |

Claws-down outperformed claws-up for the first time. Ouch.

Note that the biggest outperformance was in silver stocks. This fits, given how crazy silver went, propelling some of the riskiest silver companies higher. For example, I had owned, but sold Silver Tiger (SLVR.V) and Discovery Silver (DSV.TO) due to Mexico Risk. Both are up 4x since I sold them. Had I been less cautious, both The Independent Speculator portfolio and my claws would have averaged much better. But the new regime in Mexico could have turned out more hostile, making for a very different outcome. There was no way to be sure in advance, so I don’t regret my call. (And now, with elevated physical safety risk in Mexico, even less so.)

Copper was the next biggest miss. I was waiting for a pullback in copper stocks that did not materialize last year. This possibility is why I often rate good companies with something like: “This is a claws-down for me, but up for bulls in this space.” Regardless, my caution clearly underperformed… this time.

My claws on gold were almost even.

My claws-ups trounced my claws-downs in uranium again. This also fits, given that uranium corrected in a big way in 2025, and was highly volatile all year. Sure, it has soared recently, but it was not in anything like a manic market last year.

This doesn’t mean my claws-ups did poorly, of course. Their win rate (gains for the year vs. losses) was very high.

| Claws-Up Winners vs. Losers | Winners | Losers | Win Rate |

| Total | 92 | 8 | 92% |

| Gold | 46 | 1 | 98% |

| Copper | 12 | 2 | 86% |

| Uranium | 13 | 1 | 92% |

| Silver | 6 | 0 | 100% |

| Oil & Gas | 8 | 3 | 73% |

The win rate for claws-downs tells a different, more mixed story.

| Claws-Down Winners vs. Losers | Winners | Losers | Win Rate |

| Total | 636 | 141 | 82% |

| Gold | 291 | 44 | 87% |

| Copper | 77 | 17 | 82% |

| Uranium | 26 | 28 | 48% |

| Silver | 76 | 2 | 97% |

| Oil & Gas | 22 | 18 | 55% |

This shows that it’s still worth avoiding the losers, even in a manic market. The worst are just harder to spot when “a rising tide lifts all ships.”

Back to the bigger picture, I think it’s telling that my cautious approach underperformed the most for silver stocks. Despite my Darth Silver nickname, that’s not because I secretly hate silver. I think my aversion to political risk had much more to do with it; this concern kept my claws down on a lot of hot silver plays that soared spectacularly in 2025.

But was that really a mistake?

For those who made a different call—and cashed out—perhaps so. But if either silver keeps correcting or political risk in Latin America resurges further this year, those who didn’t cash out may still underperform.

I’m not wishing anyone ill, of course.

My point is that 2025 was an extraordinary year in many ways. I’m not planning to dump my plans to “get rich slow” and instead embrace FOMO on that—or any—basis.

I think it’s much more important to perform well over time than to be the top performer in a once-in-a-generation year.

I’m quite pleased with my 31.6% average yearly gains and my 42.9% average gain for completed trades (which doesn’t include my big wins in 2025 that are still open) documented on my public track record.

But at the end of the day, the purpose of My Take is not to recommend stocks…

We’re here to provide unbiased analysis of natural resource companies to help independent speculators make their own investment decisions.

That’s it.

If clients less risk-averse than I made more money than I in 2025, I’m all for it.

Makes no difference to my take on the challenges and opportunities facing the companies we cover.

When I see people strolling the exhibitor aisles at mining conferences with My Take on their phone or pad, asking the tough questions, I feel good about the work my team and I do.

Enough said.

Caveat emptor,