by Kyle Johnson

Mainstream economists have proven unreliable yet again. But you probably won’t hear them explain why.

Investors might want to know these facts and figures before planning their next move.

Job Revisions

On May 7, the Bureau of Labor Statistics (BLS) released its updated job data through Q3 2024. On net, the economy lost 1,000 jobs. This comes after the revisions to Q2 24 showed negative job growth of 163,000.

It might not sound too bad. But we need to compare the revised figures to the initial estimates.

On X, Danielle DiMartino Booth (formerly of the Dallas Fed) writes, “in year ended 3/31/25, [with] only two quarters of data in hand, we now know that 54% of job creation has been revised away.”

Here’s the math…

In its Business Employment Dynamics Summary, BLS reported the following initial job gains:

- +653,000 for Q2 24.

- +510,000 for Q3 24.

- +495,000 for Q4 24.

- +522,000 for Q1 25.

Total: +2,180,000.

The latest BLS revisions to Q2 and Q3 24 wiped out 1,163,000 jobs—53.3% of initial estimates for the timeframe listed above.

The BLS publishes jobs data in increments of 1,000, yet they’ve miscounted by more than one million. Revisions for Q4 24 and Q1 25 are still to come.

Unacceptable.

Even without ascribing malice, overstating job creation by nearly 54% is an indictment of the BLS. The collective silence on such an error from the economics community writ large is an indictment of the entire profession.

As a society, we’ve come to hold professionals in science and engineering to exceptionally high standards. Many are not permitted errors of 5.4%—let alone missing the mark by 54%.

Mainstream economists insist they’re doing “hard science” and demand to be taken seriously. But seemingly no error is great enough to induce the slightest bit of shame or humility. They are completely unrepentant.

Contemptible.

Consumer Spending

While government economists fiddle with their statistics, prudent investors might want to keep their eye on consumer spending.

Consumer confidence just hit a 12-year low. People are worried about their ability to maintain their lifestyle. “How much can I consume?” This is many people’s primary concern.

In my opinion, consumer spending isn’t a particularly valuable measurement of economic growth or the health of an economy. But my opinion matters very little; consumer spending drives economic policy.

The Bureau of Economic Analysis (BEA) estimates that consumer spending accounts for 68% of GDP. Interestingly, EJ Antoni (PhD economist at the Heritage Foundation) calculated that two-thirds of the increase in retail sales over the last five years is due to inflation.

This doesn’t bode well for the American consumer or the economy. Perhaps that’s why mum’s the word among mainstream economists on inflation-adjusted retail sales.

Sure, you can find stories about consumer spending here and there. But for one reason or another, legacy media outlets and mainstream economists rarely take the time to step back and look at the broader picture. Their coverage of important happenings is often superficial as a result.

Here are a few things they seem to miss.

Cantillon and Inverse Cantillon

Writing in the 1730s, Richard Cantillon discussed how an increase in the money supply affects economic actors. He rightly concluded that the people who first receive newly created money are disproportionately benefited, as they get to spend the new money before it has circulated through the economy and prices have adjusted.

Today, cozying up to the Federal Reserve is the ultimate position to capitalize on the so-called Cantillon Effect. It should be expected that the wealthy spend more than the poor. But the statistics have entered new territory—the wealthiest 10% of households account for nearly half of consumer spending. This is the highest share since Moody’s Analytics began collecting such data. And it makes sense, given that monetary and fiscal policy have supported Wall Street more than Main Street.

But I’ve long suspected that there’s also an Inverse Cantillon Effect—that signs of a struggling economy will first appear among those furthest away from the money spigot. Looking at the data, this appears to be a real phenomenon.

Discount Retailers in Trouble?

This March, the CEO of Dollar General said that many customers report only having enough for “basic essentials, with some noting that they have had to sacrifice even on the necessities.” Walmart CEO Doug McMillon says his customers are exhibiting “stressed behaviors.”

Now add tariffs into the mix.

McMillion warned of price hikes due to tariffs, claiming the company could not absorb all of the associated costs. Writing on Truth Social, Trump responded in quintessential Trumpian fashion:

“Walmart should STOP trying to blame Tariffs as the reason for raising prices throughout the chain. Walmart made BILLIONS OF DOLLARS last year, far more than expected.”

Yes, Walmart makes billions in profits. It probably can absorb some of the tariff costs to a degree. But there are limitations. Walmart operates on razor-thin margins, often reporting quarterly and yearly profit margins below 3%.

To help put this into perspective, imagine if Walmart broke even most days of the year and earned profits only from December 20–31 (11 days is roughly 3% of a calendar year).

There’s not much wiggle room for high-volume, low-profit retailers. Falling short of certain projections and benchmarks would inevitably hurt Walmart’s stock price. All shareholders would suffer, not just the Walton family.

Retail chain Target just cut annual sales projections after comparable sales fell by 3.8% in Q1. Target’s executives blamed low consumer sentiment and a “highly challenging environment” due to tariff uncertainty.

Perhaps it’s smooth sailing from here on out for discount retailers. But if that was their expectation, why would these CEOs freely offer such statements about their customers? Why warn of price hikes if they were trivial?

These CEOs are justified in smelling trouble ahead. 8.9 million Americans (5.4% of all employed workers) report working multiple jobs, a rate not seen since April 2009. Some 67% of Americans report living paycheck to paycheck. About 77% of respondents to a YouGov poll said their income is not keeping up with expenses.

Inverse Cantillon?

Looks like it to me.

Buy Now, Pay Later

You’re probably familiar with the concept of “buy now, pay later” (BNPL). Thousands of retailers have partnered with a handful of financial firms to extend credit to their customers.

BNPL has exploded in popularity.

Approximately 60% of Coachella (an annual multi-day music and arts festival held in California) tickets were purchased with a payment plan. These concertgoers are hardly the first to finance their fun. But only 18% of tickets were purchased via BNPL when the service debuted in 2009.

Concerts are one thing, coffee is another.

With apps like Zip and Klarna, coffee drinkers can use BNPL at Starbucks. Paying off a cup of joe via four installments over six weeks sounds like a Saturday Night Live skit or a dystopian science-fiction novel. But this is reality in 2025.

In March, the food delivery app DoorDash partnered with Klarna to expand BNPL options. In the first three months of 2025, Klarna’s losses totaled $99 million (more than doubling its $47 million loss in 2024).

I’m not suggesting there will be Collateralized Dumpling Obligations. It’s unlikely that people defaulting on delivery food orders will trigger a global financial crisis.

But the growing popularity of BNPL (and high rates of non- and/or late payment) is a sign of economic weakness, not strength.

A study by the Consumer Financial Protection Bureau released earlier this year found that one-fifth of consumers with a credit record used BNPL. Unsurprisingly, most of them had “subprime” or “deep subprime” credit scores.

A recent LendingTree survey found that:

- 41% of BNPL users made late payments this year, up from 34% just last year.

- 25% of respondents report using BNPL for groceries this year, up from 14% last year.

- 23% claim they’ve had three or more active BNPL loans at any given time.

Bankrate reports that 57% of BNPL users elected to pay in installments to help with their cash flow.

Perhaps BNPL is simply part of the “financialization of everything.” But it might be companies doing everything necessary to retain their customer base and prop up sales.

Either way, it sounds like an Inverse Cantillon Effect to me.

Opportunities for Rebound?

Trump and his advisors have discussed eliminating income taxes for those making under $150,000 per year. The Senate has passed a bill eliminating taxes on tips. Call me a cynic, but I’m not convinced Congress is willing to make broad tax relief a reality. If tax relief does come, I doubt it will be enough to meaningfully boost consumption.

Most Americans have relatively little saved. According to the BEA, Americans are currently saving just 0.6% of gross national income. It doesn’t seem like there’s enough in American piggybanks to boost consumption and prop up GDP.

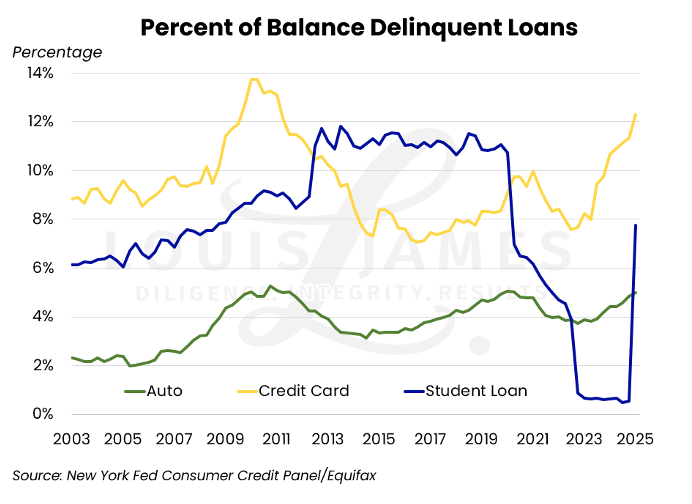

There’s turbulence in the credit markets. Earlier this month, the New York Fed released its Quarterly Report on Household Debt and Credit.

As you can see, the data aren’t pretty.

It will be interesting to track the ripple effect of student-loan defaults. Millions of student-loan borrowers recently had their credit scores slashed, making it more difficult for them to access credit.

This might not seem like a big deal, but one should appreciate the scale of debt-financed consumption. Ted Rossman, senior analyst at Bankrate, notes that consumer debt is at a record $18.2 trillion. Credit-card balances are up 54% compared to 2021. Auto-loan balances are up 19%.

Debt-financed consumption seems poised to drop. And every dollar spent on debt repayment is one fewer dollar available for consumption.

See the dilemma?

Double whammy.

Embrace Volatility

Of course, politicians and bureaucrats could let markets clear errors and malinvestments. But they tend not to have the patience and disposition to be hands-off.

So what’s a speculator to do?

Look up.

The money helicopters aren’t coming back. Lyn Alden’s theory of fiscal dominance demonstrates they never left—deficit spending won’t stop anytime soon.

Giving credit where due, Trump has done more to address waste, fraud, and abuse than any president in living memory. But the bar was set exceptionally low.

A tax and spending bill will eventually get passed. At the very least, I anticipate Congress and Trump to continue deficit spending at current levels. As Alden says, “there’s no stopping this train.”

Don’t forget that the recent tariff development with China is just a pause; nothing has been finalized. If and when there’s a deal, imports from China will be more expensive than before—that’s not going away.

Boobytraps and landmines abound. But these breed volatility. Might as well make it your friend. Now is a good time to be a contrarian speculator.

KJ

PS: Some of the deals out there have Lobo chomping at the bit. He’s eyeing uranium, copper, gold, and silver. And there’s only one place to get his latest thoughts: Speculator’s Digest—our free, no-hype, no-spam newsletter.