Gold dropped below $1,900 overnight and is headed south as I type. Generalist investors new to the space seem to be panicking, selling great gold and silver stocks indiscriminately. I’m happy to take some of those shares off their hands and have placed serval bids accordingly.

But what if gold has peaked and it’s all down-hill from here?

Then I’ll lose some money.

I’m a speculator and I’m okay with that.

I would not be okay with it if—when—gold rebounds and I leave opportunities on the table after Mr. Market came to me on my entry price targets.

What makes me so confident gold (and silver) will rebound?

It’s selling off for due to temporary—and I would say, irrational—factors. The fundamentals remain stronger than ever.

Critically, what is arguably the most important driver in the market today—interest rates—remains very bullish.

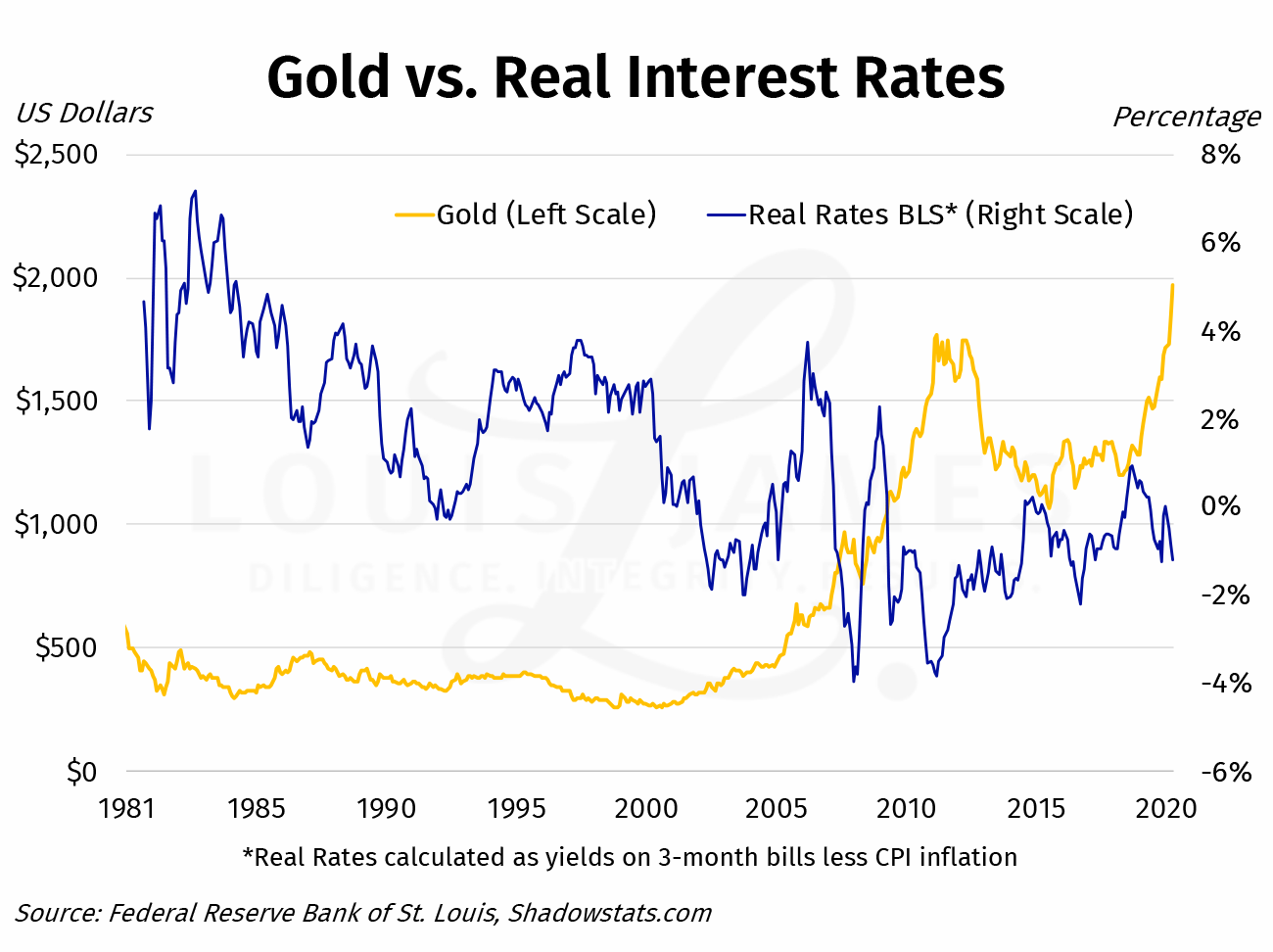

As a safe-haven asset and a form of money (if not currently in common circulation), gold has long seen its price strongly impacted by interest rates. It’s an inverse relationship. That means that the low rates in the world’s big economies are very bullish for gold.

The relationship is easy to underestimate if one looks at nominal rates vs. gold. To see it clearly, we need a chart of real (inflation-adjusted) rates vs. gold.

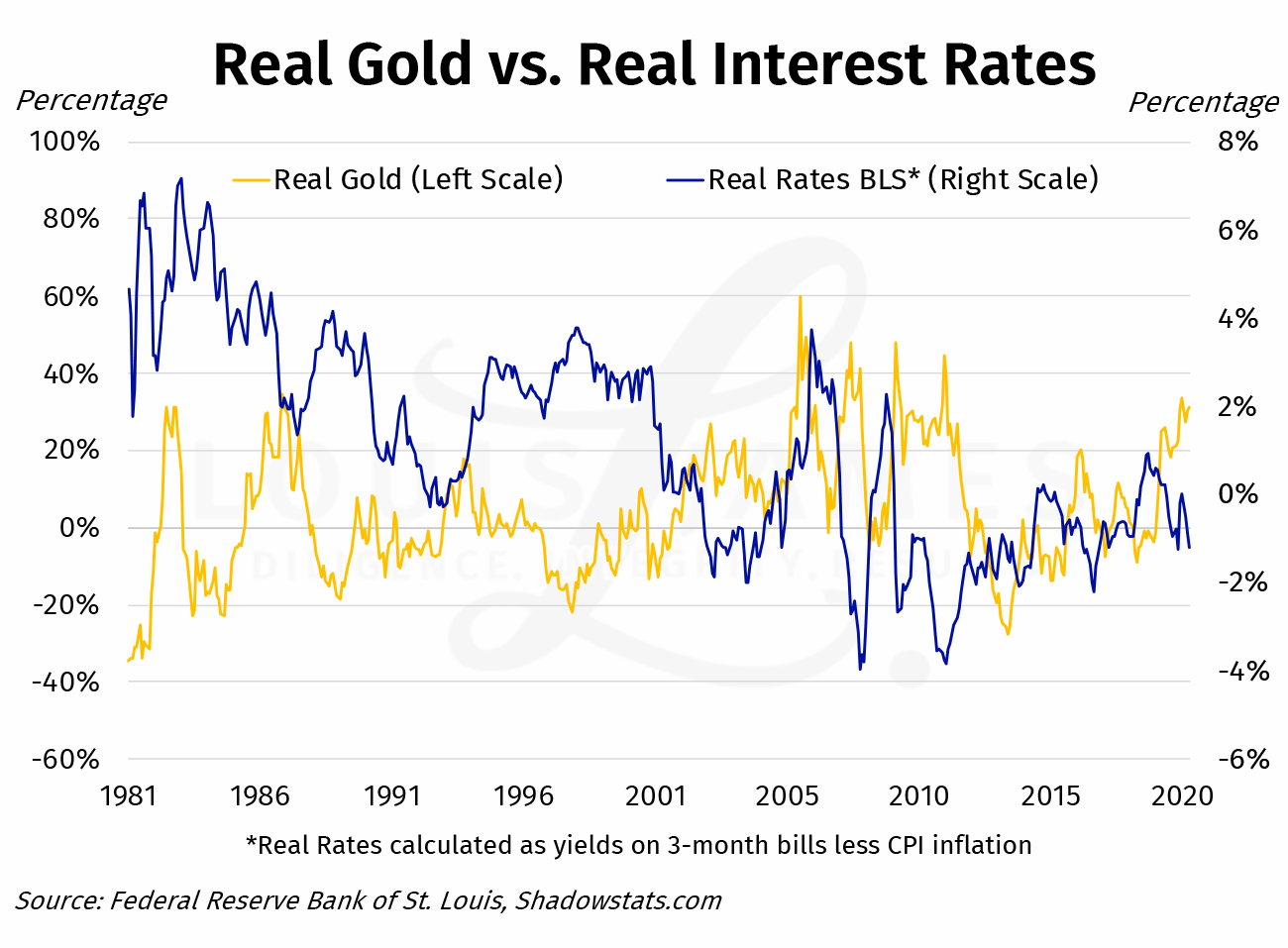

The power of this force becomes much clearer, however, if we look at real rates vs. real gold prices—that is, with both adjusted for inflation.

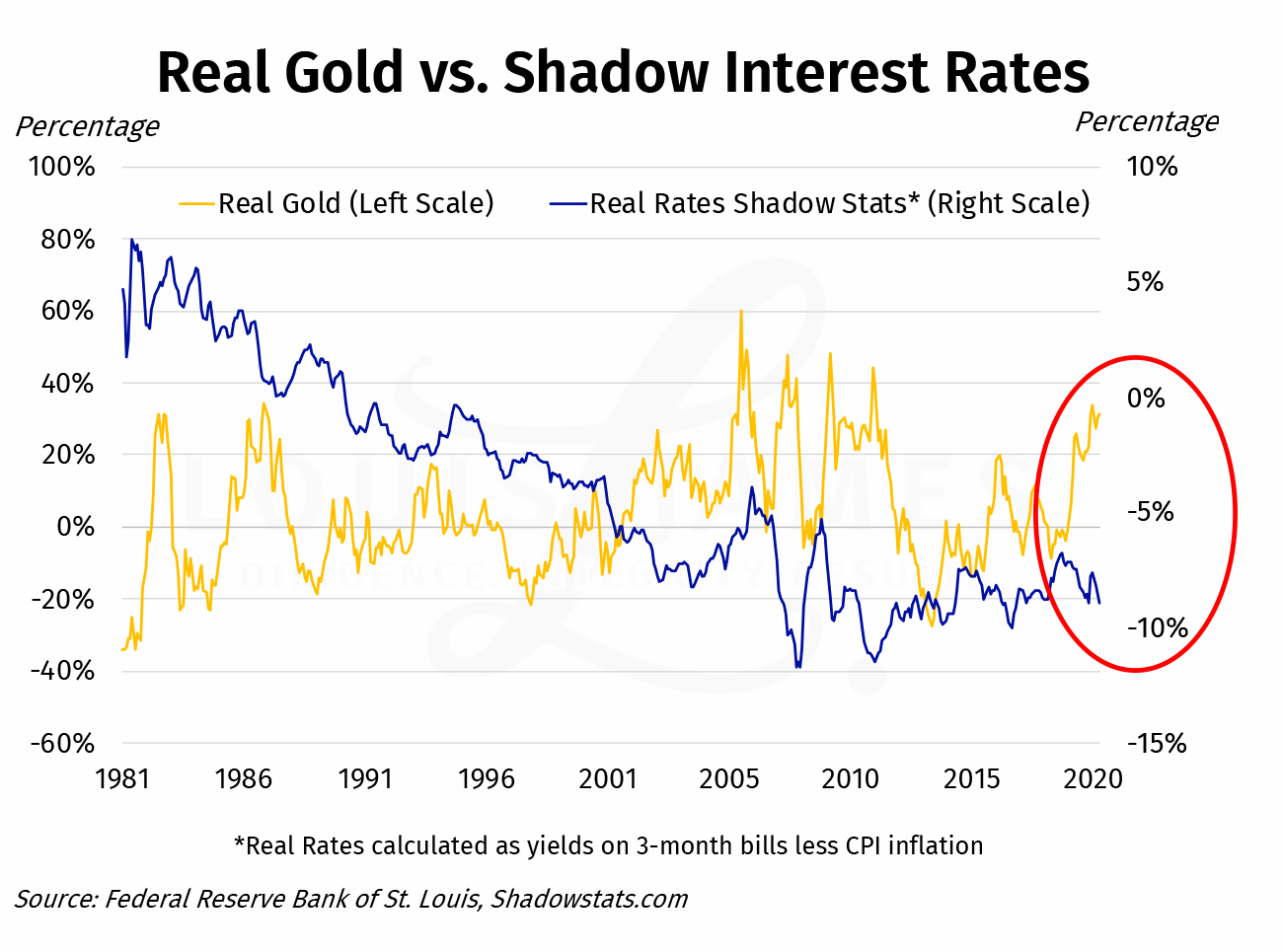

And we see this again with the added clarity regarding the long downward trend of real rates if we use Shadow Stats data. (I understand there's some controversy over Shadow Stats methodology, but the relationship is the same as in the BLS chart above.)

What makes this more than an academic issue at the moment is the divergence circled on the right side of the chart. That’s our current bullish trend. If real rates were to suddenly rise, gold would face a headwind.

But what are the odds of that happening anytime soon?

The Fed has said “no” through 2023.

The ECB… well, I’m not holding my breath.

China? They’re cutting.

And so on.

The economic realities driving central-bank policies to perpetuate the trends in the chart are one of the most solid bases for speculation that I’ve seen.

This last chart may be the single most important one for gold and silver investors to keep in mind, going forward.

This is why I think high gold prices are here to stay.

And I think much higher nominal prices are likely before they drop back to pre-crisis levels—if they ever do.

Same goes for silver, of course.

And I’m investing accordingly.

![]()

P.S. To be kept abreast of more opportunities, dangers, and issues affecting investors, please sign up for our free, no-spam, weekly Speculator’s Digest.