Given my outlook for recessionary stagflation, I’ve said that I’m only interested in gold, silver, and uranium stocks for now. This brings three critical points into sharp focus for me:

- Gold is doing well, but gold stocks remain on sale.

- Uranium is doing great, but uranium stocks remain on sale.

- Silver is… struggling. So are the stocks.

Gold

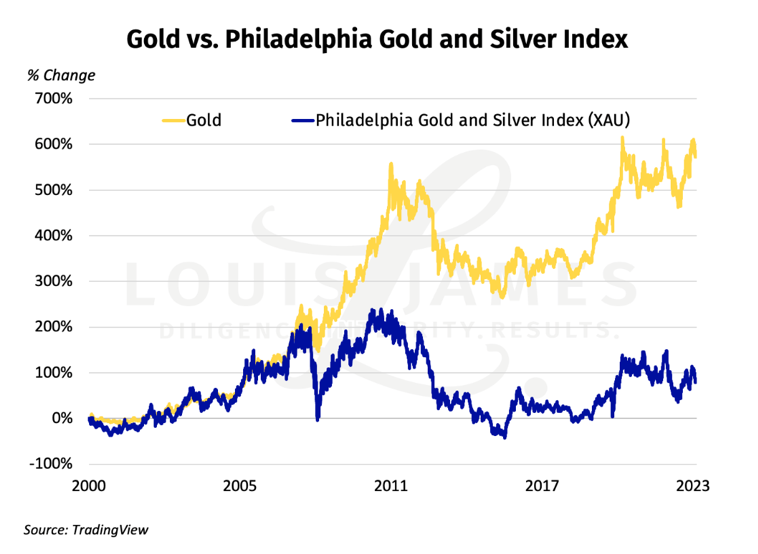

Let’s start with gold. As you can see in this chart, the stocks as a class disconnected from the metal after the crash of 2008 and have never caught up. (We used the XAU because GDX and GDXJ don’t go back that far.)

Note that the XAU is composed of mostly larger, relatively less-volatile companies. If you were reading my work back in 2008, you know that plenty of great junior companies did much better than this average performance after the crash. If I recall correctly, the picks I called Best Buys at the bottom at the end of November 2008 (published at the beginning of December) averaged something like 400% gains by the top in 2011.

Meanwhile, the XAU did rally after the crash, tracking gold, but then fell more than gold after 2011. From 2016 to 2019, it tracked gold, the gap neither widening nor closing. It rallied sharply with gold in 2020, but has since underperformed—the gap has widened despite record high gold-dollar exchange ratios.

This tells us that gold stocks are undervalued in the most real terms of all: in terms of gold.

But why?

I think there are two reasons:

- Rising costs have hit miners hard, resulting in some famous producers reporting net losses even as gold hit nominal all-time highs. No surprise that disappointed shareholders exited.

- Note that the stocks underperformed gold long before the cost issue started blowing up. As I’ve written before, I think the big driver here is fear that gold has peaked. The expectation that gold will follow the pattern it did after 2011 had investors hanging back before the lower profits. They seem even more nervous now, as the “peak” seems long in the tooth and bound to “collapse soon.”

The good news is that gold is clearly not following the post-2011 pattern.

One might say that it’s just a triple top now instead of the double top back then, but that’s already admitting that the two patterns look very different. My view is that the pattern since the 2020 surge is a plateau as gold gathers for the next big surge upward. This could happen this year, if the Fed is forced to pivot that soon.

If I’m right about where gold is going, the realization that gold hasn’t peaked should transform gold-peak fear into gold fever. That’d boost both gold and the profits of gold producers, which should finally give long-suffering gold bugs the payday they’ve been waiting for.

To leave no stone unturned, however, we should ask if gold stocks might not be “broken.” Looking at the chart above, it seems reasonable to suppose that the stocks no longer track gold. If so, they won’t deliver the leverage to the upside that’s our reason for owning them.

I can’t see that happening.

That’s not just me being a stubborn gold bug.

I don’t think it’s possible for gold stocks to underperform the metal forever; to believe otherwise requires believing that the gold companies will stay in business without ever becoming more profitable.

That’s just not the way the world works.

I think the double whammy of the COVID-19 lockdowns and the post-lockdown surge in costs is a one-off event. Once the industry gets past it, we’ll see the stocks catch up with gold with gusto.

In other words, I expect to see the “alligator jaws” in the chart above close with the bottom line snapping upward, rather than the top one chomping down.

Even if the industry as a whole underperforms, I expect the best stocks I focus on in The Independent Speculator to greatly outperform.

It may start with the go-to stocks. That’s why we call them that. But my experience in past booms is that the best of the best juniors rally just as quickly. It’s the average that takes time to move upward.

I don’t think I’m just being a Pollyanna, insisting that our gold stocks will soar despite evidence to the contrary.

In the first place, some of our stocks have soared with gold’s previous rallies and we’ve been able to take profits. My portfolio is quite different from the XAU, GDX, or GDXJ.

More fundamentally, it makes no sense to think gold can keep going higher while the stocks refuse to follow. If that did persist, management would be able to take the better companies private.

I may be wrong, but I do think we’re going to see gold break out much higher—probably this year. If past is prologue, that should set off a true market mania. But even if not, gold stocks will have a good shot at becoming the flavor of the day that delivers for those in ahead of the surge.

I’m putting my own money where my keyboard is on this.

Uranium

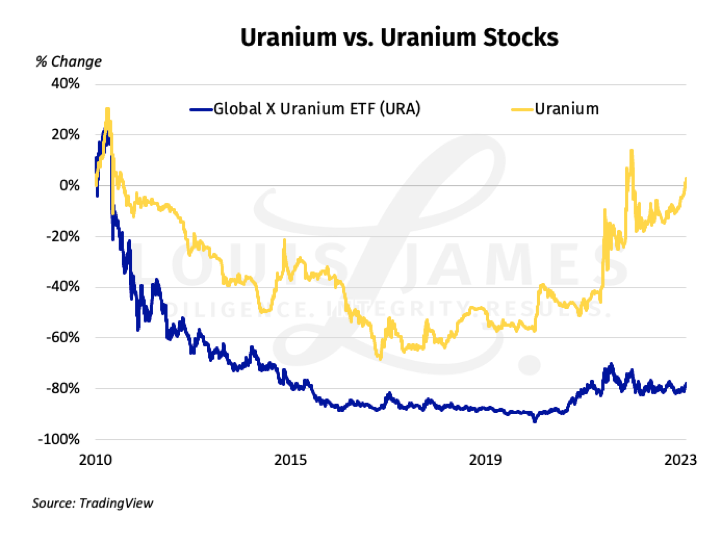

Uranium stocks have underperformed the metal itself for as long as we have an ETF to track the difference. The recent divergence, however, is even worse than for gold.

We often explain it when there’s an underperformance in uranium stocks by pointing to the broader markets being down. Uranium stocks are stocks, after all. That might seem like a worn-out excuse with the S&P 500 now “officially” in a bull market. But as we all know, the stock rally is largely concentrated in a handful of top names. The rest are trading sideways, at best.

More pertinent to uranium today is that energy as a sector shot up after Russia invaded Ukraine and has been correcting, with great volatility, ever since. The S&P 500 Energy Sector Index is down 8.3% as of this writing.

A key point, in my view, is that despite Team Soft Landing’s best efforts, most market participants expect a recession in the months ahead. Even if it’s a mild one, energy as an asset class always gets whacked hard going into a recession.

This has traders hesitant to go long uranium stocks, despite the metal having a great year. Remember that uranium doesn’t trade on the LME or COMEX.

Few have access to the metal itself, making investor sentiment visible mostly in the stocks, not spot uranium prices.

The reality on the ground could hardly be more bullish for uranium:

- The ESG tide has shifted in uranium’s favor.

- Demand from BRICS countries is already surging.

- Eastern Europe is dragging the EU toward more nuclear power—a lot more.

- Even the Biden administration has turned pro-nuclear.

- Mine supply has been insufficient for years.

- SPUT and other funds have cleaned out the spot market of cheap pounds.

- The US government has become a new end user, taking pounds off the market for its new strategic reserve.

- Power utilities are finally being forced to the bargaining table to sign new long-term contracts, and these are coming in at higher prices.

This is all happening now—and I don’t think a recession can stop it.

I may sound like a broken record at this point, but I truly believe it would take a major nuclear incident to derail the uranium trade.

I see the divergence above as a spectacular opportunity.

Uranium remains my highest-confidence trade for this year.

I’m putting my money where my keyboard is on this as well.

Silver

Ah, silver…

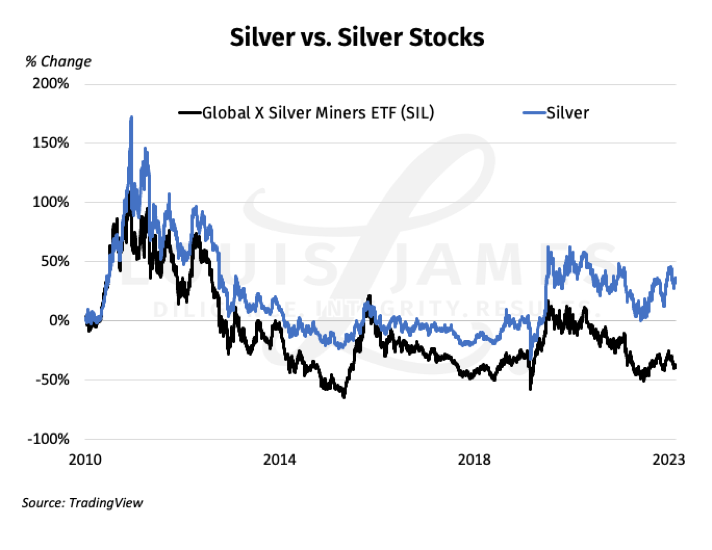

Silver stocks have tracked the metal better than gold or uranium, but that’s scant comfort when the other two metals are doing so much better recently. And the closer tracking hasn’t prevented the gap between silver and related stocks from widening this year.

Call me Darth Silver or whatever you like, but I can’t ignore how often silver has tracked copper more than gold over the last year. Assuming I’m right about gold breaking out later this year, this makes it seem likely to me that silver will underperform more than usual, at least going into the recession.

After the recession has done its worst (or Team Soft Landing has been proven right), I do think the odds favor silver more than catching up with gold.

But I have to say that I’m no longer looking to buy more silver plays until the coast is clear.

Right now, it’s just the two yellow metals for me.

If they get cheaper in the months ahead, I intend to act on the opportunities.

The fear of a 2011 repeat may make that especially hard for gold, but as long as the thesis remains intact, discipline will require follow-through.

That’s what I’m planning to do with my own hard-earned money, for now.

Caveat emptor,

![]()

P.S. To be kept abreast of more dangers, opportunities, and issues affecting investors, please sign up for our free, no-hype, no-spam, weekly Speculator’s Digest.