by Kyle Johnson

A “barbarous relic.”

That might be the most infamous anti-gold quote. But John Maynard Keynes said that of the gold standard, not gold.

Keynes wasn’t a hard-money advocate. But even if gold was not in circulation, he recognized it would serve as:

“… a store of value to be held as a war-chest against emergencies and as a means of rapidly correcting the influence of a temporarily adverse balance of international payments and thus maintaining a day-to-day stability of the sterling-dollar exchange.”

Nearly a century later, one of Keynes’ most prominent disciples would have you believe otherwise.

Dr. Ron Paul infamously sparred with then-Fed Chair Ben Bernanke about gold. Bernanke stated that gold:

“… reflects global uncertainties. … The reason people hold gold is protection against what we call tail risk—really, really bad outcomes. And to the extent that the last few years have made people more worried about potential of a major crisis, then they have gold as a protection.

RP: Do you think gold is money?

BB: [pause] No. ....

RP: Why do central banks hold it [gold]?

BB: Well, it’s a form of reserves.

RP: Why don’t they hold diamonds?

BB: Well, it’s tradition. Long-term tradition.

Technically speaking, the Federal Reserve does not own gold. The gold held in Federal Reserve vaults is owned by the US government. But it’s not a surprise that the man then responsible for issuing the world’s reserve currency denied gold’s importance.

From an ideological perspective, Keynesians see government-issued fiat currency as money. If gold is the world’s true reserve currency, that makes it the US dollar’s greatest competitor. So, practically speaking, Fed chairs can’t go around praising the yellow metal.

Imagine what signal would be sent to the markets if the Fed or US government went on a gold-buying spree. Not one of confidence. Hence, “tradition.” It’s unsurprising that official US gold holdings declined after 2001… but remain unchanged since 2006.

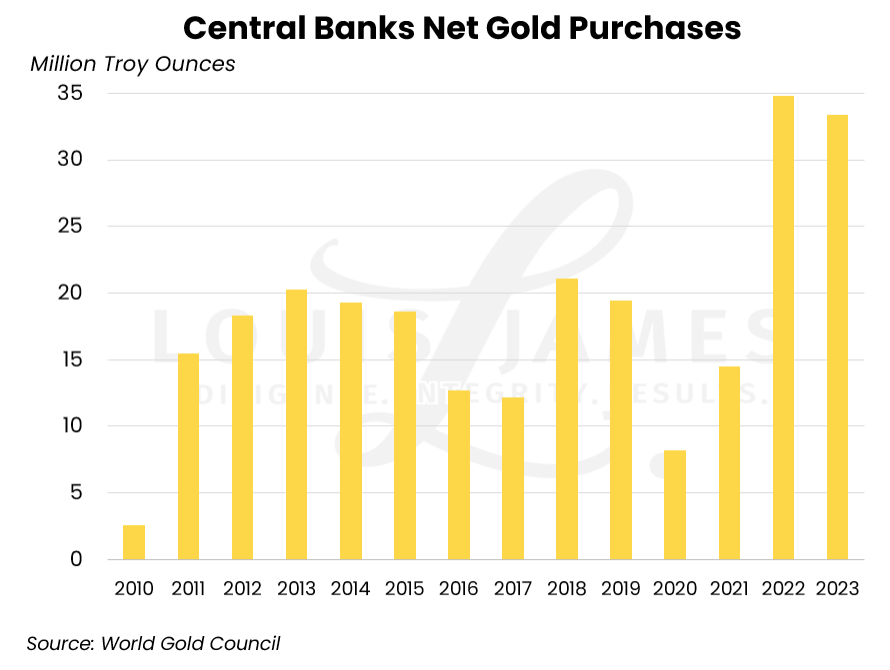

Other central bankers and governments don’t have the luxuries afforded the US, issuer of “King Dollar.” Starting in 2017, Germany, Austria, Hungary, the Netherlands, Belgium, Turkey, Poland, Czech Republic, Switzerland, Romania, Australia, Russia, and Venezuela all took action to repatriate gold. Central bank gold buying spiked in the wake of the global financial crisis. They gobbled it up after the COVID-19 crash.

Most important of all for investors today is the surge in central-bank gold-buying since the US “weaponized” its dollar against Russia. The message was heard loud and clear by central banks around the world: US dollar reserves are now risk assets for friend or foe.

Are we to believe this is all merely for tradition?

Of course, it’s not just economists and central bankers cranking out anti-gold quotes. Many investors seem to hate it—most notably Warren Buffett. He has so many anti-gold quotes it was difficult to pick just one. His comments from 2005 really stand out, however. Speaking at a conference, Buffett claimed he wouldn’t want to own gold even if the value of fiat dropped 90%. He’d prefer seashells in payment for selling candy. Buffett continued:

“Gold would be way down on my list as a store of value. I would much prefer owning 100 acres of land …, or an apartment house, or an index fund. .... I don’t see gold as a store of value. … [T]he truth is, it hasn’t worked very well.”

That’s just a head-scratcher—until you realize that Buffett is making a distinction between productive and unproductive assets. In the long run, he claims, productive assets will always win out.

Interestingly, a few years after the seashell comment, Buffett and Berkshire Hathaway became one of the biggest beneficiaries of the TARP bailout package. Neither received money directly, but many of the companies they owned did: Goldman Sachs, US Bancorp, American Express, Bank of America. One study found that Berkshire Hathaway ranked fifth among all investors in companies that received TARP assistance.

I don’t recall bullion dealers and private vaults requiring TARP funds. And I don’t recall Buffett changing his tune. But I suppose it’s much easier to be anti-gold when you’re the beneficiary of taxpayer-funded do-overs.

Notwithstanding, the “gold does nothing” mantra persists.

I’m not sure if financial journalist Jason Zweig was the first person to call gold a “pet rock.” But I couldn’t find any uses of the phrase prior to his infamous 2015 article titled “Let’s Be Honest About Gold: It’s a Pet Rock.”

With the gold-dollar exchange ratio around $1,150 (down 39% from its peak), Zweig felt compelled to trash gold. He claimed that owning gold requires a reliance on “hope and imagination.” Gold bugs, in his view, suffered from cognitive dissonance. The case for gold whispers, not shouts.

Zweig quoted former hedge fund manager and investment strategist Paul Brodsky who claimed that gold is “intrinsically worthless.” Zweig asserted that allocating more than 1.3% of your portfolio to gold is “an act of faith; it is a leap in the dark.”

Nearly a year later and with gold above $1,300, Zweig published a tepid mea culpa. He concluded by saying that “if gold shoots far up from here, it won’t be following the precedents of the past. It will be violating them.”

Four years thereafter, with gold around $1,800, Zweig published a second tepid mea culpa. He warned that anyone buying at that price ran a “substantial risk of ending up as wrong” as he’d been. Gold breached $2,000 later that year. It’s never retreated below $1,600 since.

Zweig warned that gold will suffer if interest rates rise. Well, interest rates have risen sharply, and yet gold keeps setting new (nominal) all-time highs—despite the Fed signaling “higher for longer.”

Keynes, Bernanke, Buffett, Zweig—none of them is stupid. But let’s be honest: it takes deliberate myopia to summarily dismiss gold’s 6,000-year track record.

The original J.P. Morgan said it best: “Gold is money. Everything else is credit.”

Physical gold is savings and insurance. Buy it to retain wealth, not grow it, or for use in case of great need. If gains are your goal, then consider gold stocks.

Either way, conditions are favorable. Legendary speculator Rick Rule says that global financial asset allocation has been around 0.5% in recent years. The four-decade mean is 2%. A reversion to the mean would quadruple investment demand. Hitting Zweig’s 1.3% cutoff would more than double demand.

Adding to Rick’s comment, pendulums don’t swing, reverse direction, and then stop in the middle. An overreaction to higher allocation to gold is possible—even if there is a soft landing or no landing at all.

Lobo sees a hard landing in the cards this year. I agree.

But I won't make some pie-in-the-sky gold price prediction. I’m just offering a friendly reminder that few, if any, assets do better than gold during times of chaos and uncertainty. Bullion or stocks, you probably want to own gold before it becomes fashionable to slander it once again.

KJ

P.S. Subscribe to our free, no-hype, no-spam newsletter Speculator’s Digest for Lobo’s latest thoughts on gold and the markets. You won’t find this original research anywhere else.