by Kyle Johnson

Hot or cold. This or that. In or out. You’re either with me or against me. Binary thinking is rarely realistic, and it often backfires.

You’re probably tired of hearing about the Soft Landing by now. You know the claims. The Fed is beating inflation with almost no harmful side effects. Depending on whom you listen to, the labor market is ripping—or at least chugging along nicely.

But how is the Soft Landing shaping up in the real world?

Let’s review some things economists love to ignore: energy, housing, food, and a few other important factors.

A gallon of gasoline was around $2.40 when Biden took office. It’s now about $3.55. Jonathan Smoke, chief economist at Cox Automotive, estimates that 50% of Americans are priced out of the car market (new or used). He claims half of Americans can only afford a $400 payment at most. But the average car payment for a new car is $729. It’s $528 for used. Auto-loan debt now exceeds $1.5 trillion. Delinquencies are at a 10-year high.

The median home price is $375,400. Due to high interest rates, most buyers would have a monthly mortgage rate of $2,800—up 29% compared to one year ago. Researchers studied home prices in 575 counties. They found that an average income earner cannot afford to buy a home in 99% of them.

Harvard researchers estimate someone would need an annual income of $117,100 to afford a median-price home. But the 2022 census data show the real median income was $74,580. Perhaps that will jump a bit in 2023. But it clearly won’t be enough.

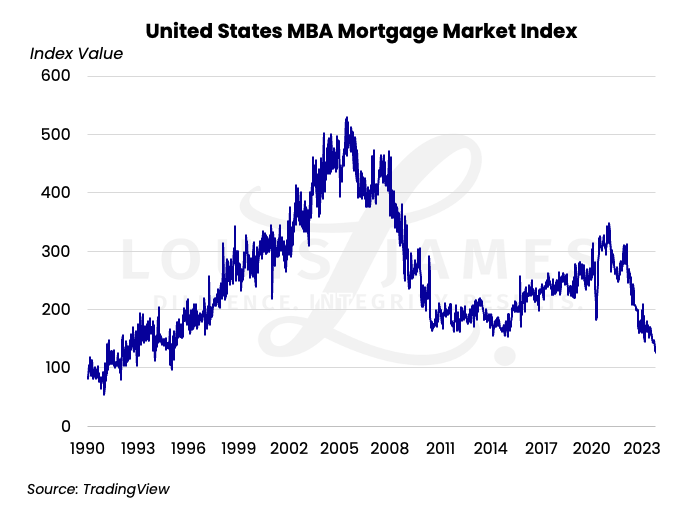

Fannie Mae estimates that US home sales will slump to 4.8 million this year, the largest sales slowdown since 2011. In August, US housing starts hit a three-year low. It seems even the wealthy are changing their behavior in response to economic conditions. Home foreclosure notices in the third quarter are up 34% year on year (YoY). The US Mortgage Market Index is hitting multi-decade lows.

The USDA forecasts that food prices will increase by 5.9% this year. The most recent data show the number of Americans receiving Supplemental Nutrition Assistance Program (SNAP) benefits is up 2.3% YoY. Nearly 42 million Americans need help putting food on the table.

US credit card debt recently surpassed $1 trillion—an all-time high. 35% of Americans carry a monthly balance (up from 29% in 2022). Delinquencies on repayment are at a 10-year high. There’s reason to suspect that many Americans now use credit cards for gas, food, and other basics.

39% of adults have a side hustle. Many report needing it to cover regular living expenses rather than to boost discretionary spending. 61% of adults live paycheck to paycheck. 72% of Americans believe they are not financially secure. Personal bankruptcy filings are up 18% YoY.

Four out of ten workers don’t contribute any money to a 401(k) or employer-sponsored retirement plan. Hardship withdrawals are up 36% YoY. The elderly are becoming homeless at a rate not seen since the Great Depression.

All of the above makes Biden’s political messaging rather curious. Biden posted to X (Twitter) that America has the “strongest economy in the world.” I suspect his economic advisors are to blame for that stance.

Janet Yellen is surprised to find “a disconnect between the numbers we’re seeing and the way people are feeling about the economy.” No kidding.

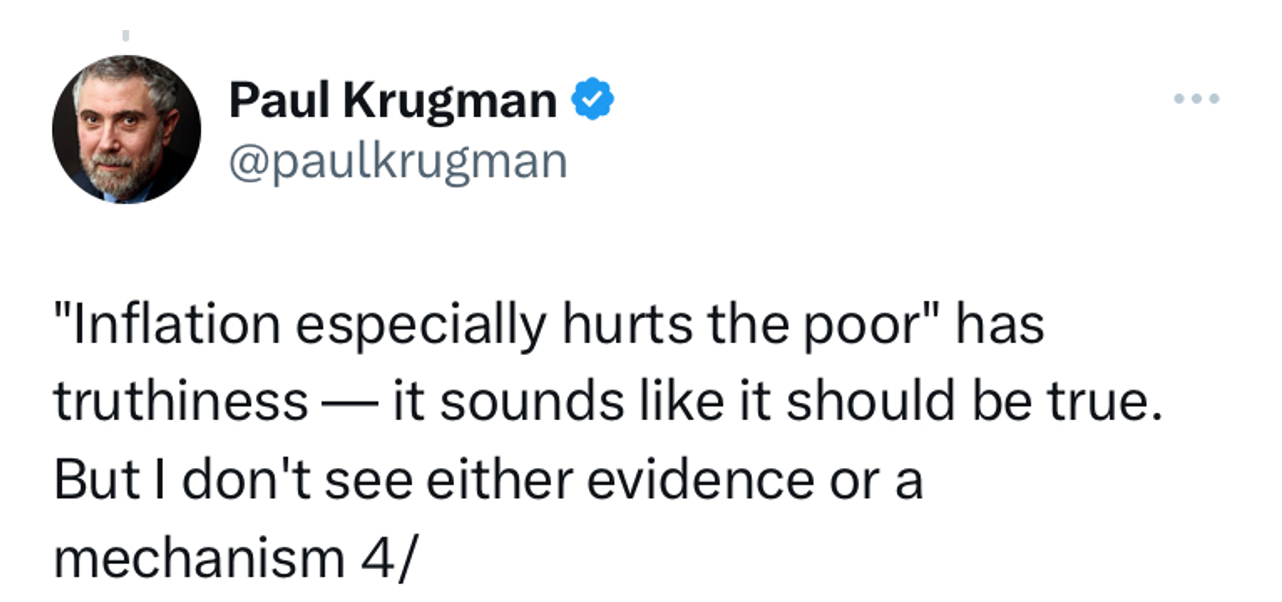

We can look to Paul Krugman to explain the discrepancy. While he holds no power directly, Krugman is a great representative of modern economic thinking. In 2021, he posted this utterly disconnected absurdity:

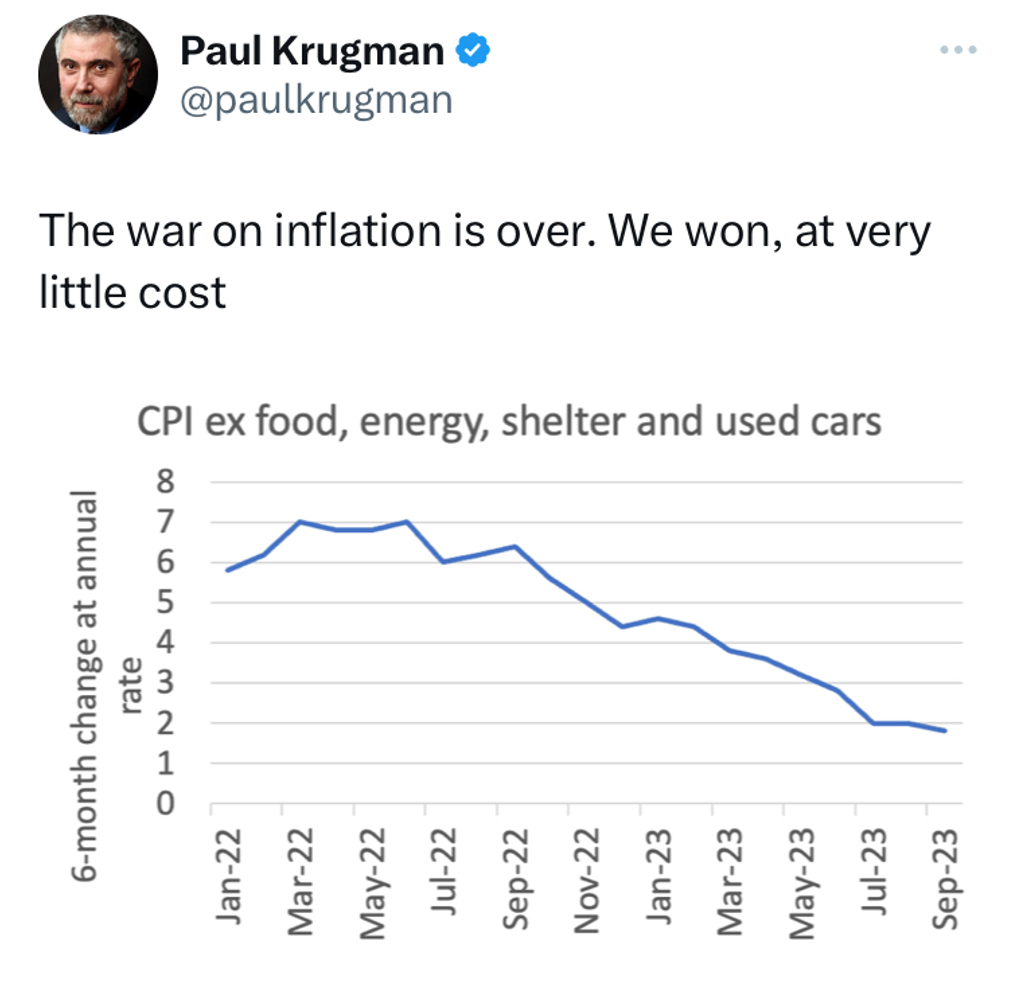

Recently, just as several inflation stats started turning upward again, he posted this statement even more disconnected from reality:

There’s no ignorance like willful ignorance.

Back in the real world, a whopping 49% of respondents to the latest University of Michigan poll claim high prices are eroding their standard of living.

Does Yellen believe people should have no preference between ground chicken and tomahawk steaks?

Does Krugman believe his willful myopia fools anyone?

There isn’t a disconnect between Americans and the data; there’s a disconnect between economists and the economy. The most highly credentialed economists shun logic and reasoning in favor of favored narratives. This arrogance is breathtaking.

There’s really no other way to phrase it.

You might recall that Ben Bernanke was once questioned on how he could prevent runaway inflation. Defiantly, he replied, “We will not allow inflation to rise above 2% or less. … We could raise interest rates in 15 minutes if we had to.”

What happened? Did Bernanke steal some of the Fed’s “tools” on his way out the door? Is Jerome Powell just stupid?

Of course not.

The blatantly obvious bias of Team Soft Landing spin doctors exemplifies the delusions of modern economists. They imagine they can pull economic levers and switches like pilots, convinced they’re in control.

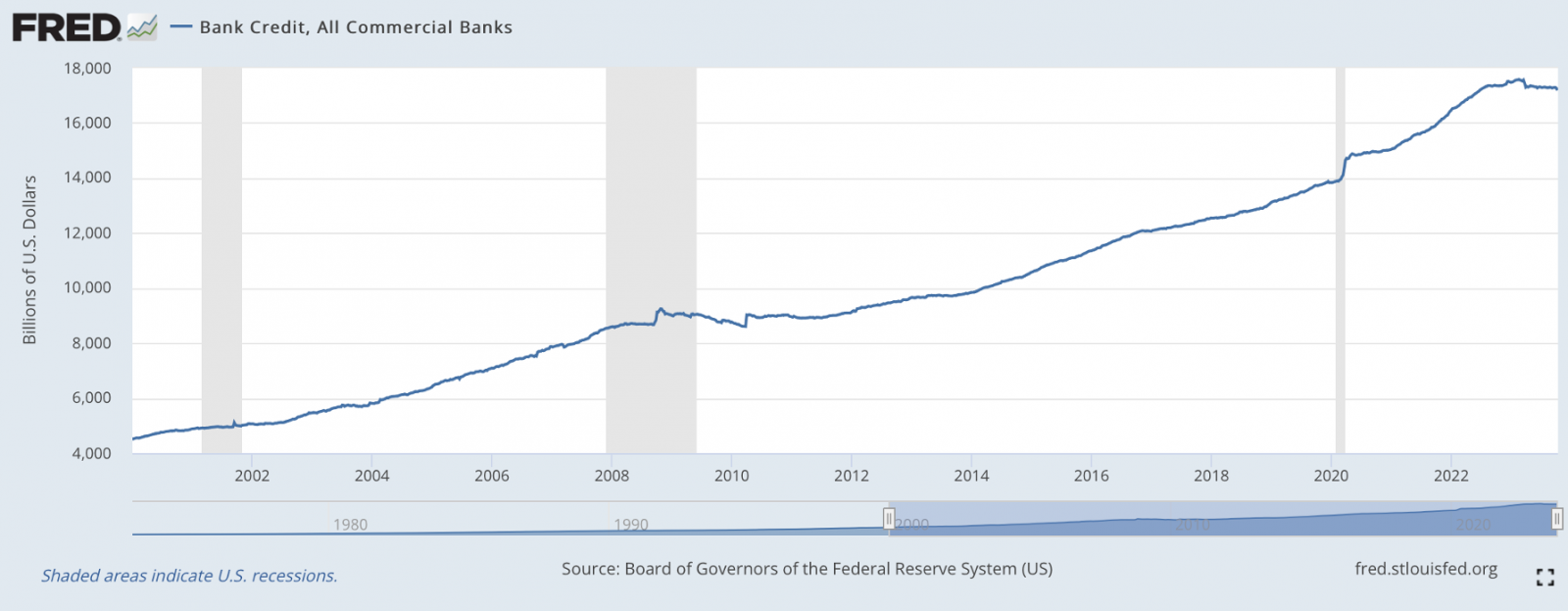

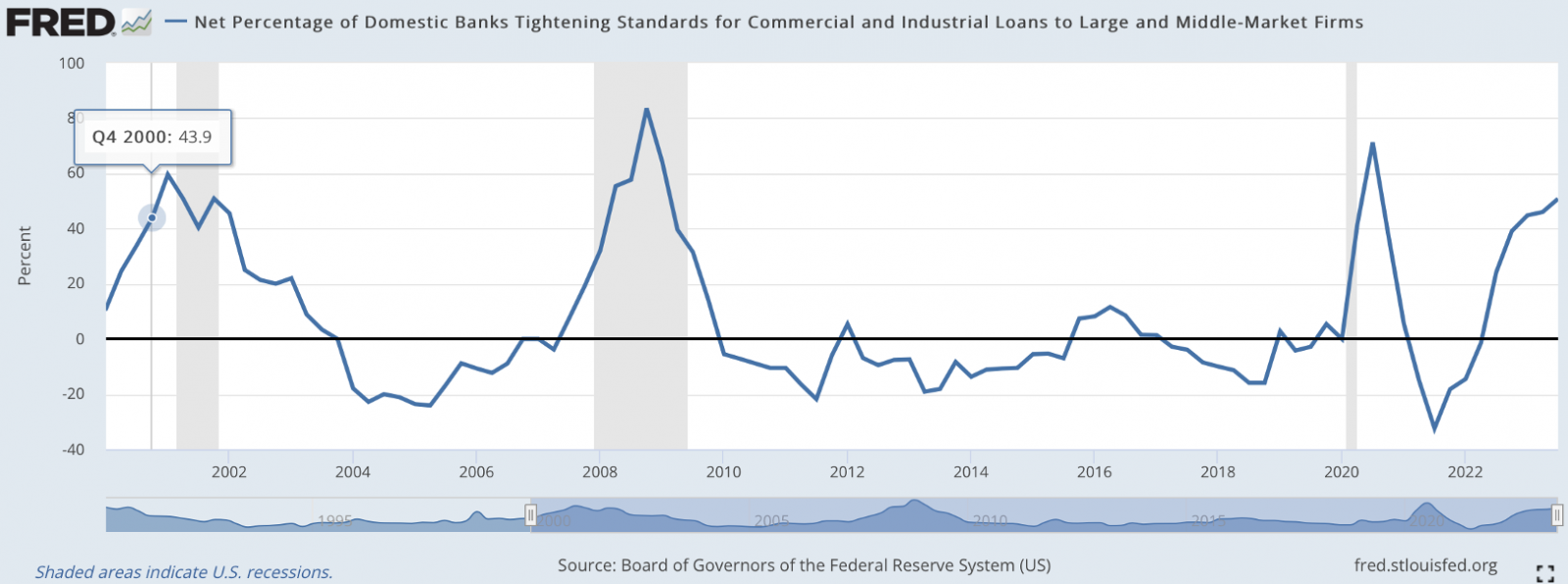

As a contrarian investor, I appreciate that many writers of like mind have called 90 of the last two recessions. I’m not trying to add my name to that list. But here is something that might have avoided your radar: rather quietly, bank credit has dipped.

Banks are raising lending standards.

Is it just me, or does this not look a lot like 2007?

That’s when the housing bubble burst. Interestingly, official data didn’t show two consecutive quarters of negative GDP until Q3 and Q4 of 2008. Of course, vast fortunes were made and lost before then.

Imagine using official GDP, inflation, and unemployment data to navigate the last recession.

Recipe for disaster.

But this can be avoided by staying patiently on the fence for a spell…

Fence-sitting is regularly used as a pejorative. It’s seen as the result of indecision… some would even say cowardice.

Neither is necessarily true.

There’s a chance Powell actually pulls off a soft landing—it’s slim, but nonzero.

A crash landing seems more likely. But being too early to an investment is often little different from being wrong.

There’s no shame in making the conscious decision to sit on the fence and wait for more data to come in. Warren Buffett’s two rules of investing come to mind.

Fence-sitting would have spared many nest eggs back in 2007 and 2008.

It might be lonely on the fence. But that’s just part of being an independent speculator. We act based on visible, if not measurable trends—not guesses.

Patience is a prime speculator’s virtue.

KJ

PS: If you want some help understanding where we are in the boom–bust cycle, consider subscribing to our free Speculator’s Digest. It’s the only way to receive Lobo’s latest thoughts on the latest economic and market trends—with no hype or spin-doctoring.