by Kyle Johnson

Santa called seeking help with his list regarding some big players in the world of economics and finance (plus one name you might have never heard before). Here’s what I told him.

Janet Yellen

Another year, another underwhelming (if not maddening) performance from Yellen as Treasury Secretary. It was mostly filled with mushy-worded cheerleading about “the strongest economy ever.” This “labor market expert” couldn’t tell you what would happen next. But every step of the way, Yellen was reassuring everyone that everything was going according to plan.

In March, Yellen confessed “I regret saying that [inflation] was transitory.” But I suspect she regrets the statement due to the hassles it caused her. She ought to regret her lack of understanding of economics that led to such a gross error. But instead we got more “tweaking” of models rather than destroying them root and branch.

This month, Yellen made a last-ditch attempt to escape the naughty list. During the Wall Street Journal’s CEO Summit, Yellen admitted:

I am concerned about fiscal sustainability, and I am sorry that we haven’t made more progress. I believe that the deficit needs to be brought down, especially now that we’re in an environment of higher interest rates.

This is a stark change of tune.

From March 2023, “I think the path that’s set out in the President’s budget is fiscally sustainable.”

In September 2023, Yellen was “not really concerned about the impact” of spending on the debt and deficit.

Last July, she said: “If the debt is stabilized relative to the size of the economy, we’re in a reasonable place.”

Well, unemployment peaked (officially) in July at 4.3% and now sits at 4.2%. Although it’s currently rebounding, the CPI is down from 2.9% in July.

Did the economy shrink? Did we go into recession?

Not according to Yellen. In September, she claimed there were no “red lights flashing.” A blurb from a Bloomberg piece reads:

“While there are risks, it really has been amazing to be able to get inflation down as meaningfully as we have” while maintaining strong growth, Yellen said in Austin. “This is what most people would call a soft landing.”

But now Yellen sees a problem with the debt and deficit? What gives?

Yellen was sworn in as Vice Chair of the Federal Reserve on October 4, 2010—the national debt was $13.6 trillion. Since then, Yellen also served as Fed Chair and Treasury Secretary. The debt now exceeds $36 trillion. Who has played a more prominent role in the economy during this time?

She’s been steering the economy with a foot on the gas pedal, covered eyes, and plugged ears. Yellen has access to the best information. She could pick up the phone and talk to just about anyone in finance and economics. Yet she is completely dismissive of her detractors.

The damage she’s caused cannot be undone by a flippant “oopsies” of an apology.

She has zero humility.

Zero self-awareness.

Zero shame.

Recommendation: Naughty, and, if you see fit, urge her to permanently abandon positions of power and the public spotlight.

Jerome Powell

Fed chair isn’t an easy job. Not only do people judge your every word, they also judge your intonations and gesticulations.

I don’t envy him.

Markets could crash if Wall Street believes him to be insufficiently optimistic. Without a doubt, Powell must bite his tongue regarding the games being played behind the scenes with other key figures (like US commercial banks, US politicians and bureaucrats, foreign banks, other central banks, etc.).

Personally, I’m thankful Powell doesn’t have Bernanke’s arrogance. I like that he doesn’t copy Greenspan’s intentionally confusing and verbose style of FedSpeak—something Greenspan openly called “syntax destruction.”

Overall, Powell is relatively inoffensive.

But he does miss the mark sometimes. Like in May when he said, “I don’t see the stag or the flation.” Or in November when he said “the whole plan is to not have stagflation. That is actually our plan.”

Hopefully, this was just bluster and he does appreciate the dangers of stagflation. Good thing for him, perfection is not a prerequisite for the better half of Santa’s list. And credit where due, we haven’t crash-landed.

Recommendation: Nice, though his present should be modest.

Austan Goolsbee

As president of the Chicago Fed, Goolsbee is familiar with Chicago’s brutal winters. It seems his modern furnace is broken and that he wanted to secure enough coal to stay warm the old-fashioned way.

This month on X, a video was posted of a horse trainer pretending to bridle a horse. Despite the bridle not actually being there, the horse responded as though it were (turning and changing speed as “instructed”). A question accompanied the video, “What is this called in psychology?”

From what appears to be Goolsbee’s personal X account, he replied “forward guidance”—a reference to public statements from Fed employees about the future course of monetary policy and, by default, the economy.

His honesty provides a glimpse into the mindset of the people behind the curtain. But if this snarky reply did in fact come from Goolsbee himself (and not an impostor), it’s a bad look for Fed officials. If not, I stand to be corrected and apologize accordingly.

Recommendation: Naughty, pending confirmation.

Erika McEntarfer

As commissioner of the Bureau of Labor Statistics (BLS), she is ultimately responsible for the statistics published by the agency. She’s also responsible for protecting them until their official release.

Tough to deny that it was a bad year for McEntarfer. A million-or-so jobs have been revised out of existence—so far. Certain financial firms (allegedly called “Super Users” by a BLS employee) reportedly gained early access to information.

McEntarfer’s public statements are few and far between. I find that unacceptable given what took place with BLS statistics in 2024. For better or worse, the BLS holds a critically important position in our financial system. As head honcho, she should not be allowed to lurk in the shadows.

Put a mic in front of her and let or shine… or put her foot in her mouth. Let the markets dissect her command of the issues at hand.

Recommendation: Naughty, with enough coal to make the public wonder why.

Zippy Duval

You might not have heard of Duval before, but he’s president of the American Farm Bureau Federation (AFBF)—a tax-exempt agricultural lobbying organization. This year, they published a report claiming the average Thanksgiving feast for 10 people costs just $58.08.

The claim was not that it was possible to spend just $5.80 a person, but that this was the average cost.

For reference, the most recent information lists $5.69 as the US national average for a McDonald’s Big Mac (no fries, no drink).

Holidays are a time for celebration (which are excessive by definition). Do what you must to make ends meet. But nobody who was able celebrated the holiday among family and friends for just $5.80 per person.

I recommended Santa send his helpers to snoop on Duval and his closest friends to see how much they spent on their Thanksgiving meals. He should be in big trouble if it’s above $5.80 per person.

Recommendation: Naughty.

Claudia Sahm

It was a tough year for this supposedly “pre-eminent” labor market economist. Sahm threw away “her” rule on a whim and refused to address previous errors and omissions—all the while imagining she nailed every subtle move in the economy.

She’s one of many prominent economists who need to put up or shut up.

Recommendation: Naughty, with dishonorable distinction if possible.

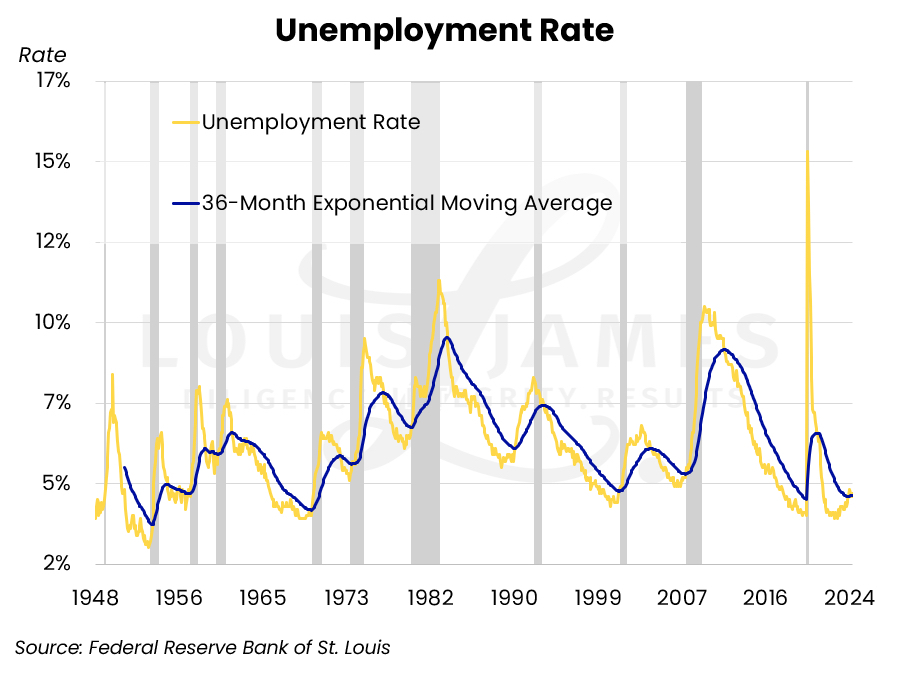

Jeffrey Gundlach

There was no equivocation from this Bond King regarding his most-trusted recession indicator: when unemployment crosses above its 36-month moving average, we’re in recession.

Look closely and you’ll notice it has a perfect track record for the last 80 years… until September when the “Gundlach Indicator” (as Lobo calls it) was triggered.

The National Bureau of Economic Research (NBER) gets the final say as to when recessions are officially recognized. Their call is made retrospectively, and so far the NBER says there’s been no recession. So either “this time is different,” or the books have been cooked.

Unlike Sahm, Gundlach stuck to his guns. That takes fortitude.

Recommendation: Nice.

Lyn Alden

One of Alden’s claims to fame is her macro thesis of Fiscal Dominance—that huge deficit spending (even when times are good) can overpower monetary policy. She came up with this thesis long before 2024, yet it’s never been more relevant.

In my opinion, Fiscal Dominance combined with voodoo performed on official statistics explain why the Soft Landing vs. Hard Landing debate drags on.

Recommendation: Nice, with special accommodation for being one a few macro analysts worth following.

Modern Monetary Theorists (MMTers)

Another year goes by during which MMTers fixate on word games. If you’re unfamiliar with their cavalier approach to rhetorical liberties, consider watching the documentary film titled Finding The Money (which was released in late 2023). Spoiler alert, it was terrible.

For the cast and crew, 2024 should have been spent addressing their strongest critics (and the steel-manned version of their arguments). But that doesn’t seem to be of much interest to Stephanie Kelton, Pavlina Tcherneva, Mathew Forstater, L. Randall Wray, Fadhel Kaboub, Lua K. Yuille, et al. But flippant responses to partial reconstructions of arguments abound.

“Heads I win, tails you lose”—MMTers offer some form of this statement whenever asked for clarification or a rebuttal. Satisfied with themselves, they plow onward imagining every criticism has been dispatched, rather than side-stepped.

Recommendation: Naughty, despite the risk of them engraving the coal and mistaking it for money.

Joe Biden

Biden’s 2024 was one of the strangest years ever for a sitting president. But I’m going to limit my commentary to the economy.

Biden’s actions on the economy in 2024 were par for the course: borrow and spend. Kick the can down the road. Create problems for future generations to solve. Dishonorable behavior.

Do his ride-or-die supporters truly believe it was a good idea to give Rivian (a failing luxury EV manufacturer) a $6.6 billion loan? Especially when established brands are pivoting.

Politicians lie. So it’s no surprise that Biden’s messaging on the economy was deceptive… except in September when called the Inflation Reduction Act “the most significant climate change law ever.” That admission was humorous and refreshing.

Perhaps Biden drinks his own Kool-Aid, or believes it necessary to bolster his legacy. But his economic messaging did not change after he dropped out in July, nor after Kamala Harris lost in November. He continues to promote the idea that in 2024, America has the “strongest economy ever.”

I’m not naive enough to believe Biden is the one controlling his social media accounts. But he is ultimately responsible for the ridiculous claims published to them (particularly on X).

From the @JoeBiden handle, he’s still claiming 16 million jobs were “created” during his presidency. But of course, this figure counts from the bottom during the worst of the COVID-19 crisis and includes millions of people returning to their old jobs. Hardly creation.

In the same X post, he claimed that since taking office, “our economy has grown more than during any other presidential term this century.”

Multiple PhD dissertations could be written on the absurdity of this claim.

From the @POTUS handle this month, he is still promoting Bidenomics as “middle-out and bottom-up.” Interestingly, Reuters just reported that in 2024 the number of American billionaires jumped from 751 to 835 (with their estimated total wealth going from $4.6 trillion to $5.8 trillion).

I’m not going to claim this is a bad thing. But I’d bet every penny I have that Biden would if it occurred during a Republican’s presidency.

During the year, polls showed that a record number of Americans claiming inflation was their number one concern. A poll by Primerica’s Financial Security Monitor found that two thirds of middle-income Americans felt they were falling behind due to rising costs. Many people, including millions of Biden voters, have struggled to make ends meet or make significant progress toward their financial goals. No amount of statistical manipulation and braggadocious assertions alter economic reality.

Recommendation: Naughty.

Jared Bernstein

As chairman of Biden’s Council of Economic Advisers, Bernstein must take responsibility for Biden’s out-of-touch messaging.

But that wasn’t the worst. Nope. The low point for him was a viral clip of him struggling to explain how the treasury market and monetary system work. Granted, it was from a documentary released in 2023. However, the clip went viral this year and Bernstein did nothing to clarify his statement or display competence on the matter.

Embarrassing on all accounts.

Recommendation: Naughty.

Uranium Investors

2024 started white-hot for “the other” yellow metal. Everyone was happy. But uranium spent the rest of the year cooling off.

Prudent and patient investors focused on hunting down good deals, keeping the longer-term thesis in mind. Unfortunately, other uranium investors did little more than complain that 2024 wasn’t a repeat of 2023.

They should turn their frowns upside down. The AI energy boom is real. Environmentalists are capitulating and jumping on the nuclear bandwagon. China leads the way in new reactor construction. Many countries are moving to restart currently dormant reactors. Things are looking up for years to come.

Recommendation: Nice (assuming they did more than complain).

Gold Bugs

Hard to imagine how things could have gone much better for gold bugs in 2024—the gold-dollar exchange rate (as Lobo likes to say) is up over $700 from this year’s lows. I lost count of how many times it hit a new nominal high.

Admittedly, some gold stocks did not respond as gold bugs might hope. Their performance is so puzzling, many wonder if gold stocks are broken. Well, let’s just say gold bugs shouldn’t give up now after coming so far.

Recommendation: Nice.

Silver Bugs

2024 was the best year for silver bugs in recent memory. Silver spent a significant portion of the year above $30 and nearly broke $35 in September.

Undoubtedly, some silver bugs were happy to finally unload after buying at some point during the bull run beginning in 2009. But silver bugs are a tenacious bunch. Many more remain in the trade, and for good reason—the bull case remains unchanged. Silver is positioned for another solid year in 2025.

Recommendation: Nice.

Copper Investors

Given our economic outlook at the beginning of the year here at The Independent Speculator, copper did better than we expected. It now has our full attention.

The metal jumped from about $3.80 per pound in January to over $5 in May. As I’m writing this, it now sits at about $4.20. Investors who capitalized in 2024 deserve recognition and praise. An impressive feat given the murkiness clouding our precise location in the boom-bust cycle.

Recommendation: Nice.

One Last Thing

Given Donald Trump’s re-election, there will be some turnover to the cast of characters pulling the strings and calling the shots on our economy. But that doesn’t mean our current problems will up and vanish after his inauguration.

Regardless of your opinion on the incoming administration, Santa, I urge you to stay vigilant in your monitoring of our public servants.

KJ

PS: Uranium was Lobo’s highest-confidence trade of 2023. Gold was his early pick for 2024. And for 2025? Lobo’s highest-confidence trade is copper. There’s only one place to learn how he’s approaching it, the Speculator’s Digest—our free, no-hype, no-spam newsletter.