My friend Doug Casey calls mining a “crappy, 19th-century choo-choo train industry.”

For years, legendary speculator Rick Rule has spoken about the chronic underperformance of gold mining companies. He points out that from 2000 to 2010, the gold-dollar exchange ratio was up more than sevenfold. And yet, free cash flow (FCF) per share among Philadelphia Gold and Silver Index (XAU) companies declined. This, he says, “took real skill.”

I bring this up because I hear from long-suffering gold bugs that they’re worried their stocks might not live up to their hopes and dreams in this new bull market for monetary metals. That’s not unreasonable, given gold miners’ track record of fumbling opportunity.

This is likely at least part of why the alligator-jaw chart of the divergence between gold and gold stocks never closed during the gold rally of 2020—and it’s been widening ever since.

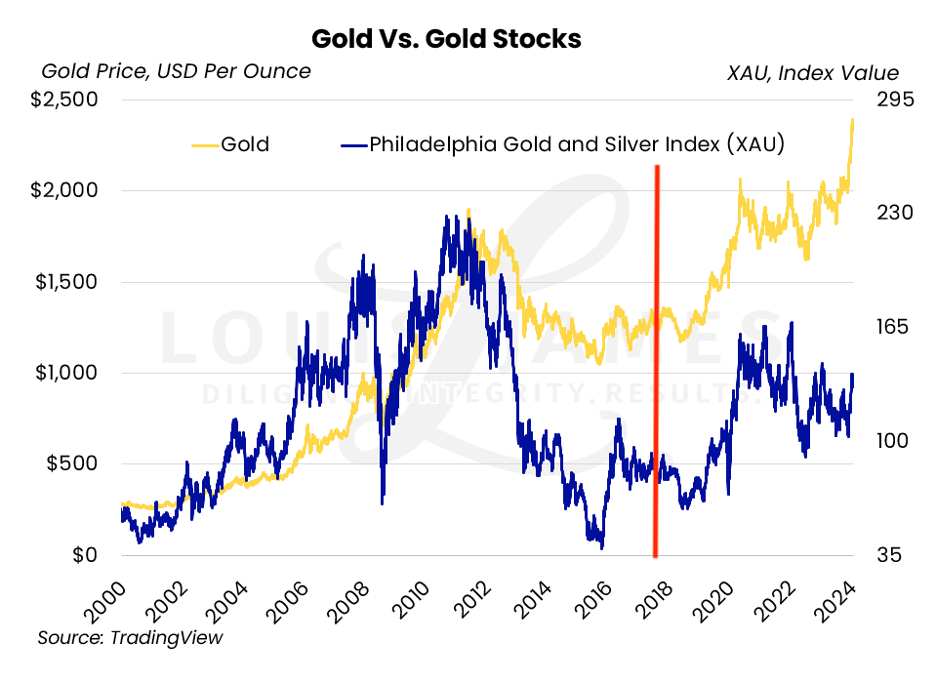

I’ve put a vertical red line on this chart of gold vs. gold stocks to show when things seemed to change. To the left of the red line, gold stocks show more volatility than gold, both to the up- and downside.

The jaws opened wide during the 2011–2015 bear market, which was painful but normal. The jaws started to close in 2016 when the stocks rallied much more than the underlying metals. (I remember First Majestic going up 5x in early 2016—while still losing money.) This too was normal. It’s exactly why we speculate on mining stocks. The whole idea is to catch the greater volatility to the upside when gold rallies (or on a discovery if one has a lot of play money and can afford to be very patient).

However, to the right of the red line, gold stocks continue showing more volatility than gold to the downside—but not to the upside. Hence the widening of the jaws… as alarming to gold bugs as the higher gold-silver ratio is to silver bugs. This is not normal. Even so, it remains painfully clear in gold’s recent breakout to new (nominal) all-time highs.

The fact is that though the divergence started in 2018 in the chart above and despite the series of higher highs in gold, gold stocks have been trending roughly downward since 2020.

Rick is surely right that smart investors remember gold miners as a group failing to deliver value in the last major bull market. In addition, I think the big money in this space (still) thinks gold spiked in 2020, and its next big move will be down. The stocks have been “leading” gold ahead of an expected bear market. I think that expectation is wrong. (More on that in a moment.)

What happened in 2018? Nothing market-changing that I can lay a claw on. As for market psychology, I think the big head-fake gold and silver rally in 2016 is likely a strong factor. It just took a while for the dreams to die and the disappointment to sink in.

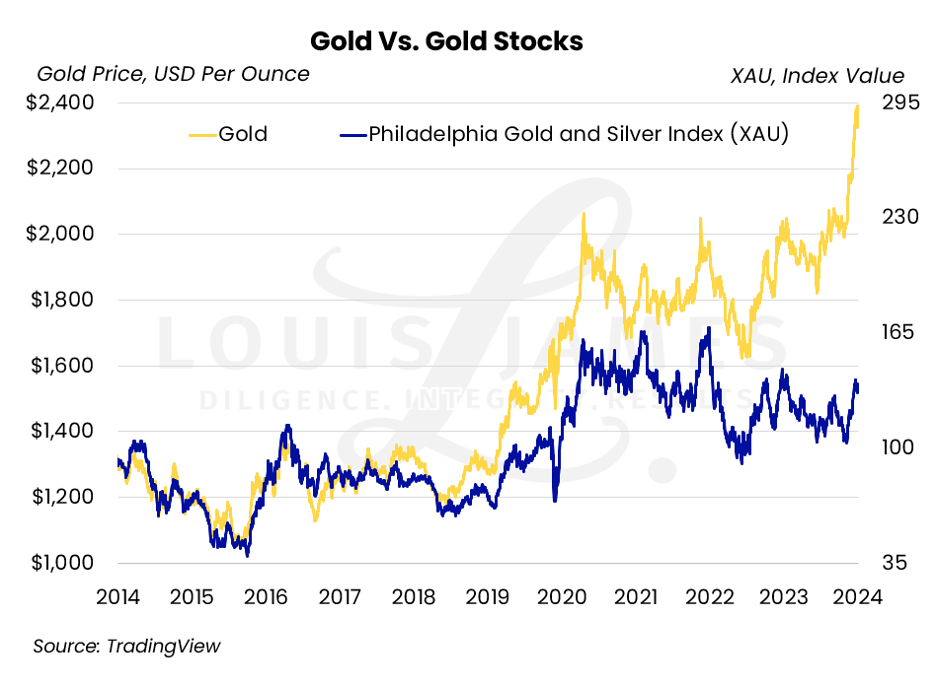

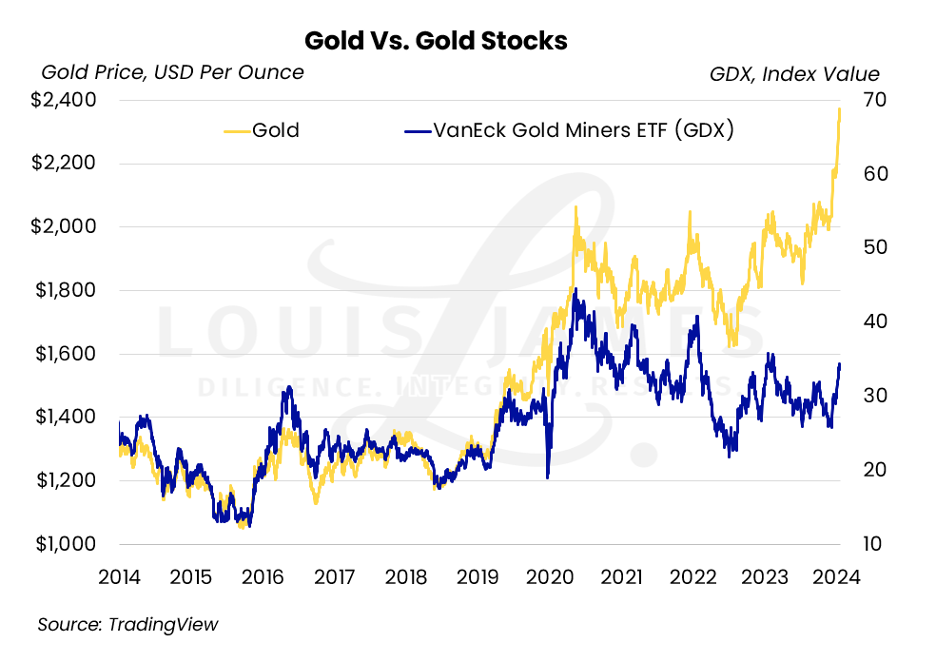

Also, the XAU is not the entire universe of gold stocks, nor is it necessarily representative. If we look at the VanEck Gold Miners ETF (GDX), the disconnect looks more like a 2019 thing.

Whenever and whyever it started, the divergence is still there. The downward trend in the stocks since 2020—while gold itself is rising—is even more painfully evident.

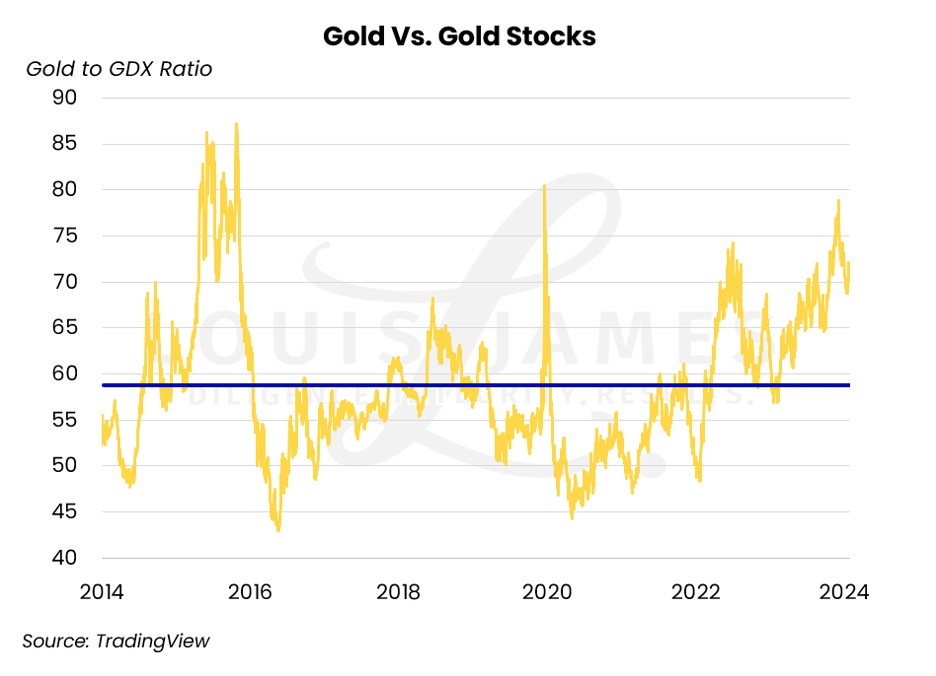

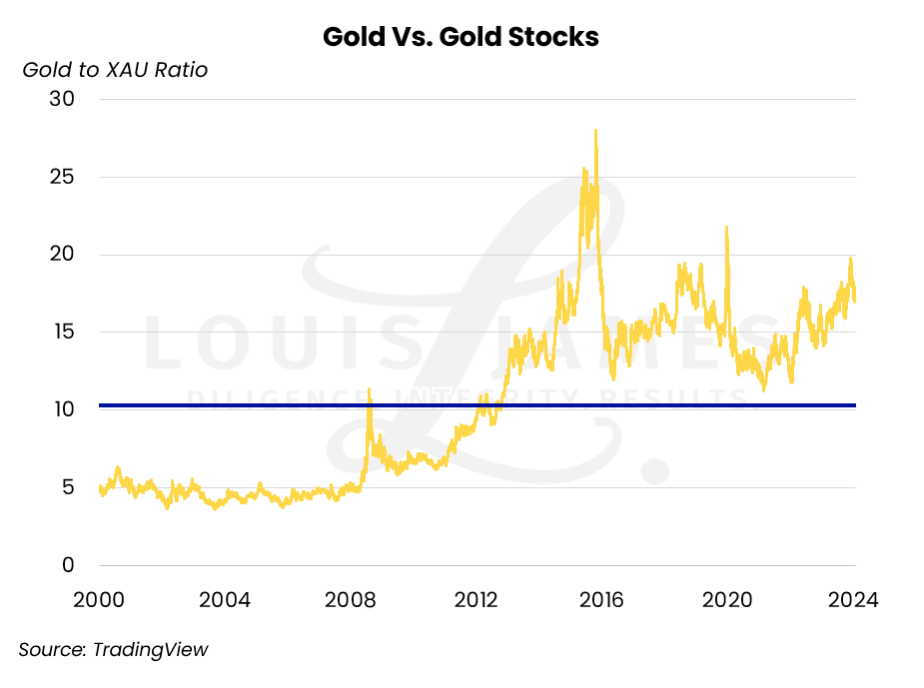

Another way of looking at this is to look at gold vs. gold stocks as a ratio, the same we look at the gold-silver ratio. As you can see in this chart of gold vs. the GDX, the ratio is worse than average (higher is worse)—and it’s been trending that way since 2020.

If we look at the same thing but use the XAU to get a longer time frame, we see a huge breakdown between gold and gold stocks just before the “head fake of 2016.” That was the multi-year bear taking anti-gold stock sentiment to an all-time high. The big rally in H1 2016 instilled new optimism, but not enough to take the ratio back below its long-term average. Then things got worse again, until 2020 instilled some new optimism—which has now faded and the trend is negative (upward) again.

I can’t prove it, but I think the main factor rubbing salt in this wound is that the central banks buying gold to hedge against the US dollar are not buying gold stocks. Why would they? They’re not in it to speculate on higher prices. They’re looking for protection, which gold has excelled at for thousands of years.

The pile-on is made all the worse by junior mining stocks no longer being “the most volatile securities on Earth,” as Doug used to call them. Momentum-chasing volatility junkies now have cryptos and tech stocks to offer them the thrill of gambling on the greater fool theory.

So, are gold stocks a broken asset class?

Could it be that the market has changed, and this time they will never catch up to gold?

In modern parlance, are we done here?

No.

Markets do evolve over time. This market’s psychology is clearly more skeptical of gold stocks than it has been in the past. But neither human nature nor the basic math of business have changed. The latter tells me that if most producers—perhaps even just the most high-profile producers—do turn higher gold into higher margins, investors will pile in. The former tells me that money always flows to where it’s rewarded.

This combination is very bullish for gold stocks… if the producers don’t flub it again.

But will they?

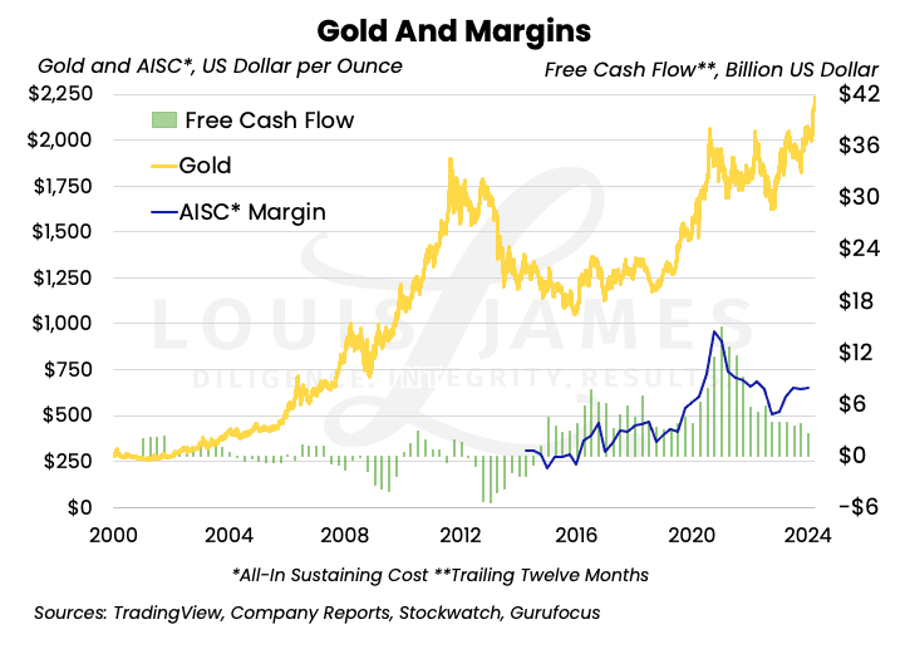

I’m cautiously optimistic. That’s not because I’m a gold perma-bull, but because the latest data show the world’s top gold producers driving costs lower after the 2020 lockdown spike.

All-in sustaining cost (AISC) is a new metric, implemented when kleptocratic governments kept raising taxes on miners based on operating margins. So we’ve shown AISC as far back as we could go, and FCF even further back. As you can see, Rick’s right about miners generating negative FCF for much of gold’s previous big rally. However, they mended their ways, with FCF trending up from 2013 to 2016. Fortunately, FCF also surged in 2020 and 2021, covering much of the higher AISC at the time.

AISC seems to be stabilizing, but FCF has fallen recently (though it remains positive). Why, if costs are steady?

I’m sure that share buybacks and dividends are part of the reason, and both should be attractive to investors. But I suspect that it has more to do with reinvesting cash into new mines and expansions, to make good on record (nominal) high gold, going on four years now. That’s even more bullish for companies investing in their own futures.

This is why I’ve said in recent interviews that the financial results of the quarter just completed will be very important for the gold sector.

If the miners allow more cost blowouts and squander the opportunity to deliver greater value to investors, the stocks may well remain in the doghouse for longer.

But the chart above suggests that they should deliver wider margins. This may or may not impress meme-stock chasers, but it should be attractive to Big Money that understands basic business math.

What if the companies deliver but investors don’t reward them?

I don’t think that’s likely. It would contradict my perception of human nature. Even if it did happen for a time, it wouldn’t last long. If miners start gushing cash and no one notices or cares:

- They’ll start boosting dividends. Strongly positive real yields from miners counter that old saw about gold “not paying interest.”

- They’ll buy back a lot more shares, which would boost earnings per share and should boost share prices.

- Ultimately, if the market simply refuses to recognize stellar performance by management of any company, they will amass treasuries large enough to take their companies private. That’s not an ideal exit strategy for shareholders… unless they get to enjoy even greater profit distributions within those newly private companies. (After all, they’d have to vote for the change, so management would have to offer them incentives.)

Speaking of momentum-chasers, it’s also possible that even if gold miners flub it again, gold could become such a viral flavor of the day, the stocks would soar anyway. (For example, First Majestic in 2016.)

Consider what happens if inflation remains sticky around 3%—or heads back north again when base effects peter out in a couple months…

Powell was careful not to say he’d beaten inflation, but the dot plot says he and the FOMC thought they had—and now they’ve pivoted to a more hawkish stance. If they’re forced to hike again instead of delivering the three cuts their guidance says “will likely be appropriate,” Powell is going to come across more like a Burns than a Volcker.

Add to this Team Soft Landing’s widespread expectation of a mild recession in the US this year—never mind the hard landing I think is coming—and the 2020s start rhyming a lot more with the 1970s.

Stagflation.

Burns rides again.

“Everyone” knows what happened to gold the last time it was like this in the US.

Now, I did use that dangerous word “if” several times in this regard. I’m not predicting this outcome. I’m just saying it’s a card in the deck we’re playing with.

Meanwhile, the Fed is still signalling rate cuts this year. Historically, rate-cutting cycles are good for gold. And while no one can say how long central banks will remain net buyers of gold, the decision many countries have made to diversify out of the dollar is very unlikely to be reversed. This is very bullish.

These things tell me that—even without the hard landing I still expect in the US—gold is likely to trade higher later this year.

And if we do get that hard landing while inflation remains elevated… hold on to your hats.

That’s fun to think about, but it’s not the main thing I’d like you to take away from this article.

My point is that the financial results now pending from gold producers could be just the thing that stops the underperformance of gold stocks this year.

It may not help much if gold goes into correction mode again until the Fed starts cutting—or is forced to hike because it failed to tame inflation—but the smart money will notice. A profitable business will attract capital. It always does.

This is why I’ve been saying I expect the alligator jaws to snap shut, with the stocks catching up to gold, rather than the other way around.

That’s my take.

![]()

P.S. I’m also very bullish on uranium, and I do see the current correction as a terrific source of opportunity for those looking to get on board. As always, no arm-twisting, but anyone interested in getting a regular update on my outlook without a flood of daily advertisements is welcome to sign up for my free, weekly Speculator’s Digest.